Asia fuel oil sold off sharply in June, with HSFO down 23.6% and VLSFO down 17.6% month-on-month, as the US-Iran risk premium gradually comes off after the signing of US-Iran Memorandum of Understanding (MoU). The month's real story was divergence: HSFO fell hardest on expectations of Strait of Hormuz and Middle East Gulf high-sulphur normalization, yet through most of June the grade stayed physically tight due to disrupted Russian supply amid continued Ukrainian drone strikes. VLSFO proved far more resilient, holding its crack on tight low-sulphur blendstock (rising gasoline crack pulled blendstock into secondary units) and widening its premium over HSFO (Hi-5 spread) to a month-end $161/MT. The East-West arbitrage narrowed for both grades as the Singapore sell-off outpaced Europe. Market will observe whether actual Russian supply loss keeps the prompt supported or expected Strait of Hormuz normalization flips market balance to excess supply.

Market Activity

- HSFO window flipped to strongly buyer-dominated (4.67 bid/offer ratio), a regime change from May’s seller-led window; VLSFO also bid (2.84 bid/offer ratio).

- VLSFO window also bid (199 bids vs 70 offers) on thin execution (10 trades); Glencore was both top buyer (29) and top seller (42), intermediary positioning rather than directional flow, with the buy-tilt consistent as blendstock tightness supported cracks.

- HSFO 380 CST window strongly bid (252 bids vs 54 offers, 35 trades), reversing May’s offer-dominated, seller-led window (Chimbusco, Mercuria offering); buy-side dominance against a -23.6% flat-price month reflects prompt supply tightness from absent Russian barrels and validates a crack that stayed positive most sessions, with bids led by PetroChina (70) and Union (56) as refiner coverage, Vitol (65) positioning, and Aramco SG bidding (45) notable as a Middle East Gulf producer-trader buying rather than supplying.

Price Action

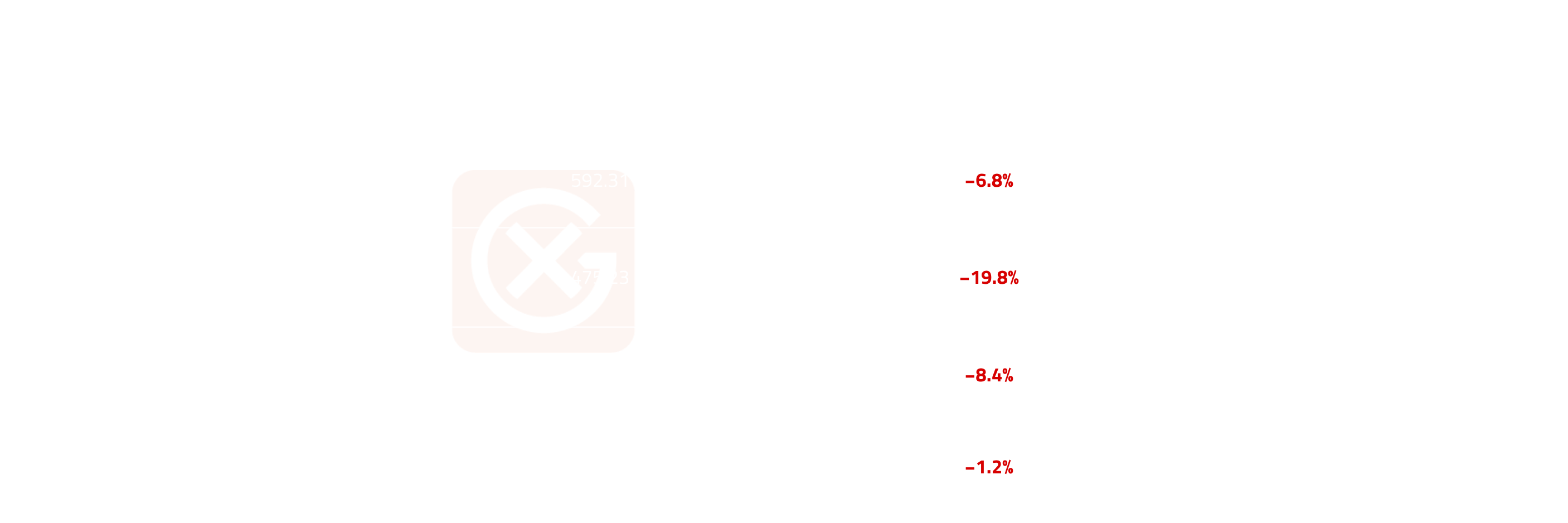

- VLSFO opened $751.16/MT, closed $588.96, and averaged $655.32 (−17.6% MoM, +27.6% YoY); HSFO opened $645.45, closed $427.72, and averaged $519.91 (−23.6% MoM, +16.3% YoY); intra-month range HSFO $225.32 vs VLSFO $195.48.

- Largest single-day drop for both grades was 12-Jun (VLSFO −6.1%, HSFO −6.9%), following the announcement of US-Iran MoU to be signed; W3 the breakdown around the 17-Jun signing, with W4-W5 moderation (HSFO −1.2% into month-end) signaling tentative support, not retracement.

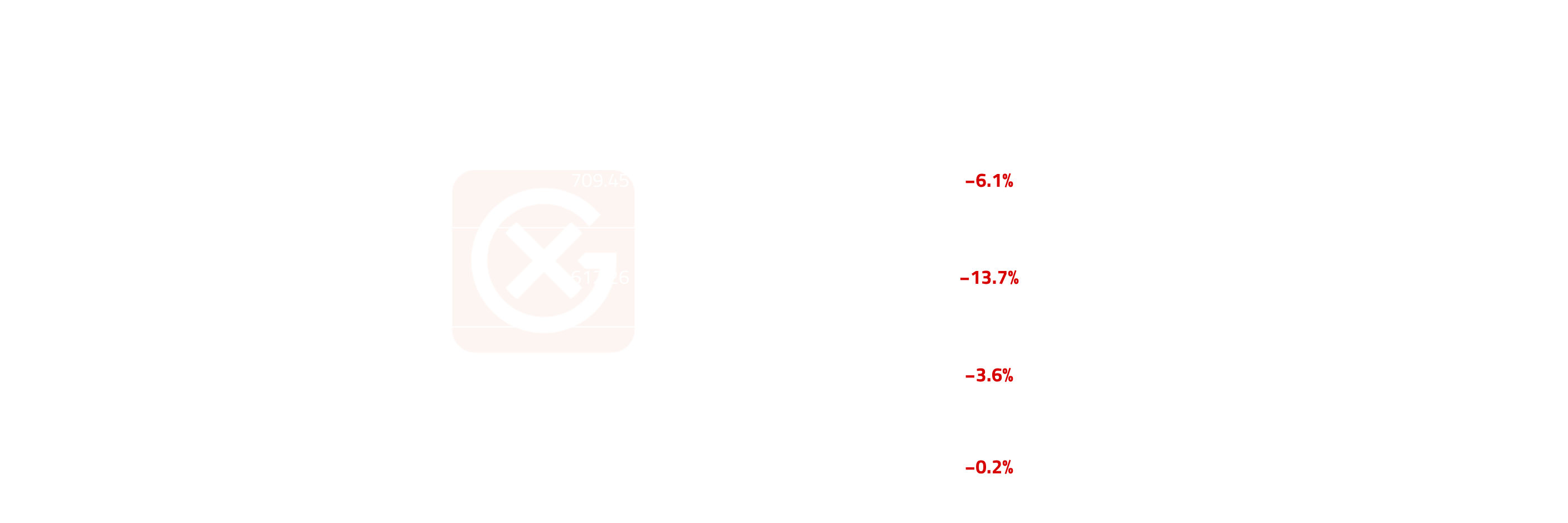

380cst HSFO FOB Cargoes (USD/MT)

0.5% VLSFO FOB Cargoes (USD/MT)

Cross-Market Dynamics

- HSFO crack held positive most of the month before slipping negative into the close while VLSFO crack held firm on blendstock tightness; Hi-5 widened to $161/MT.

- HSFO vs Dubai crack narrowed from $8.85/bbl (open) to −$0.93 (close, 30-Jun), averaged $2.48 vs May’s $3.93 (−$1.45 MoM), with the trough at −$2.74 on 22-Jun; it held positive through most of the month, the compression and late flip pricing expected Gulf normalization, while the earlier positivity reflected absent Russian barrels.

- VLSFO vs Dubai crack held firm ($25.49 to $24.46, avg $23.80 vs May’s $22.00, range $20.15–$26.16) on tight low-sulphur blendstock; the divergence widened Hi-5 from $105.70/MT (open) to $161.24 (close), peak $164.29 on 19-Jun, avg $135.40 vs May’s $114.76.

Cross-Regional Dynamics

- HSFO East-West spread compressed from +$80.70/MT (open) to +$21.97 (close, 30-Jun), avg $35.57 vs May's $54.51 (−$18.94 MoM), nearly closing at +$1.82 on 23-Jun; the Singapore premium eroded as Strait of Hormuz flows normalisation hit Asian HSFO harder than European barges, shutting most of the incentive to pull high-sulphur barrels East.

- VLSFO East-West spread also narrowed, from +$133.16/MT (open) to +$51.46 (close), avg $84.97 vs May's $99.10 (−$14.13 MoM), but held materially wider than HSFO throughout, consistent with VLSFO blendstock tightness keeping Singapore's premium over Europe more intact.

Curve Structure

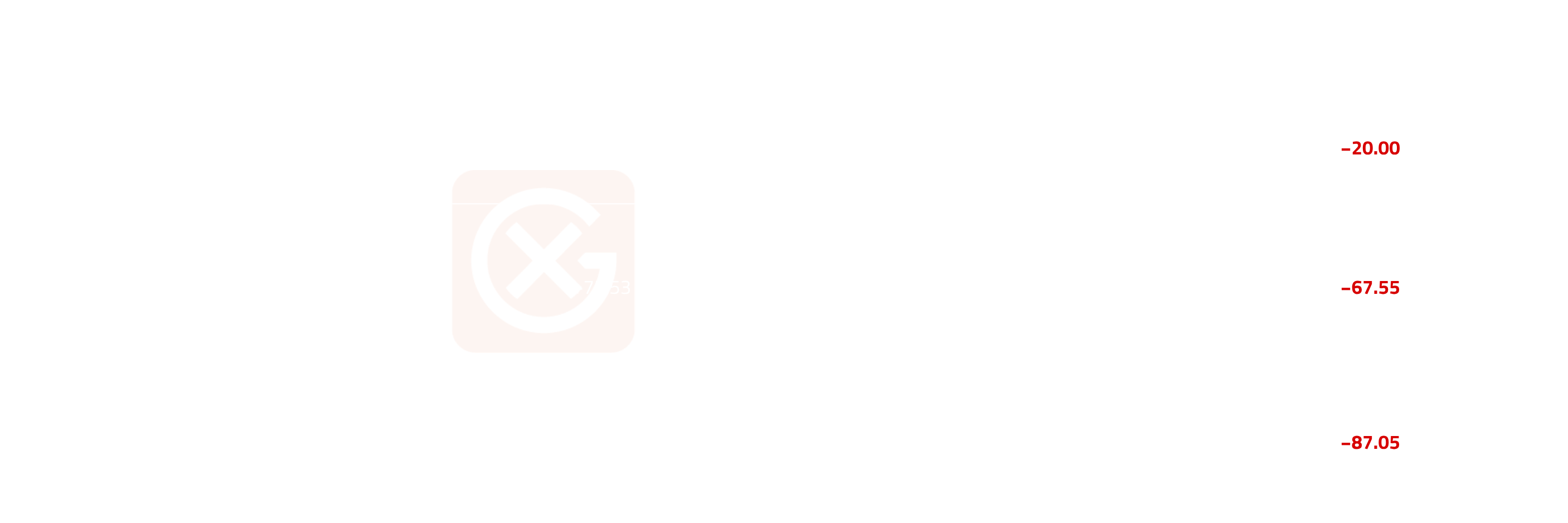

- Sharp flattening of backwardation on both grades: HSFO the violent case (M1 −$152.20 vs M12 −$68.56), its M1-M2 backwardation collapsing from +$19.50 to −$0.50, a flip into slight contango that marks the prompt now marginally oversupplied as the market prices Strait of Hormuz normalization and return of Middle East Gulf high-sulphur supply; VLSFO retained backwardation (M1-M2 +$22.75), consistent with blendstock tightness holding its prompt up relative to HSFO.

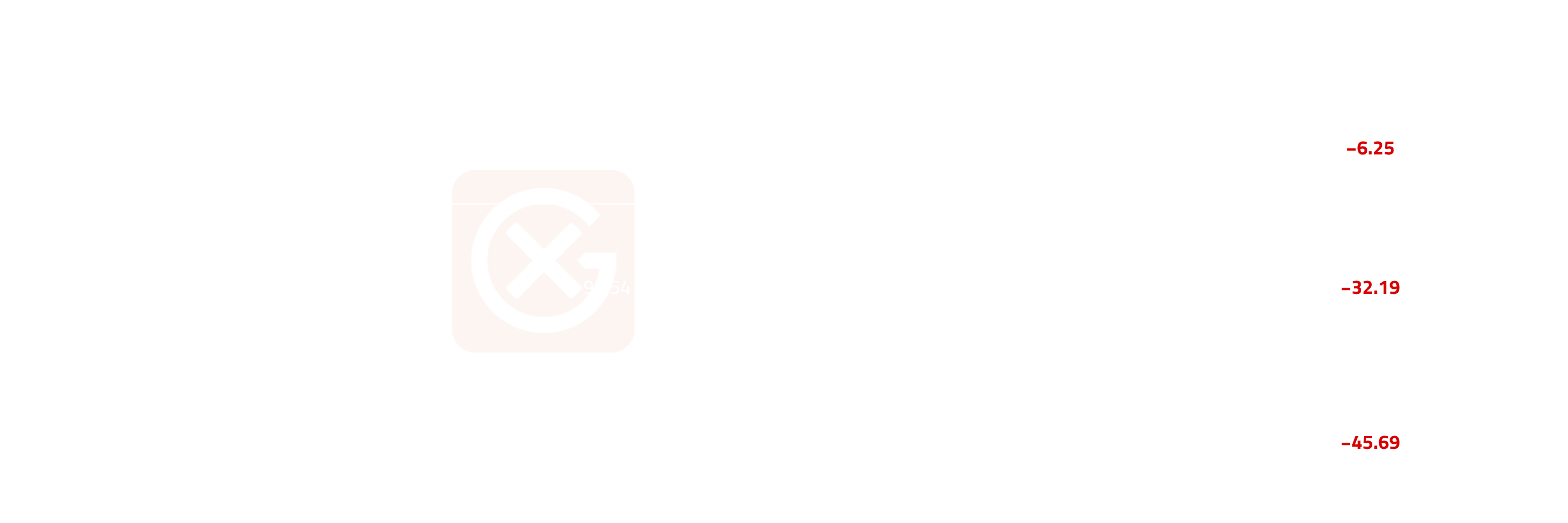

380cst HSFO swaps (USD/MT)

0.5% VLSFO swaps (USD/MT)

Price Volatility

- HSFO June Coefficient of Variation (CV) of 16.20% exceeded its March reading (12.70%) and was the highest in the six-month window, on the violent front-led repricing in swaps against still-tight prompt physical; VLSFO’s 10.55% was second only to March (14.93%), the gap consistent with blendstock support dampening its swings.

Something to Watch

- Lower Russian refinery runs amid continued drone attacks by Ukraine are expected to be supportive for HSFO crack, though Middle East supplies will eventually cap the HSFO crack strength as the Strait of Hormuz traffic normalizes.

- Dangote’s Residue fluid catalytic cracking (RFCC) unplanned turnaround helped relieve prompt low sulphur blendstock supply; bullish for VLSFO crack if the issue can be resolved in time, as the Nigerian refinery is incentivized to capture the elevated gasoline cracks.

Note: All figures, prices and market activity referenced in this report are based on the period 2-30 June 2026.