Singapore middle distillates values fell for the month of June, with jet and gasoil flat prices tumbling over 17% and 18% on the month as easing Middle East-related supply fears took the risk premium out of crude. Cracks to Dubai crude dipped MoM but at a slower pace than flat prices, pointing squarely to crude as the driver rather than any significant shift in product fundamentals. Across the month, curve structures flattened sharply from backwardation and volatility crept back up, though nowhere near March's conflict-driven extremes. Regional flows adjusted too, with India jet cargoes pivoting toward Africa while arb windows between Northeast Asia and the USWC held open.

Market Activity

Swaps

June saw 151 Gasoil swap trades done within the month at 1.01 million metric tons, a healthy step up from May's 137. The standout story is a complete reversal of direction from Dare Global Limited. After building a strong net long position through May, Dare flipped to a dominant net seller in June, accounting for 64.2% of total Gasoil swap sales (97 out of the 151 trades). Strong purchasing activity from Dare was confined to the first half of the month (16 buy trades clustered between June 2 and June 16) before they sold continuously through to June 26, selling roughly 81 lots (4,050 KB) on Gasoil.

On the buy side, Vitol Asia was the most active accumulator at 22.5% of traded volume, ahead of Gunvor (12.6%), Dare (10.6%), Axil (9.9%) and Onyx (9.3%). Vitol ended the month with the largest net long at +1,400 KB.

Jet swaps were notably more balanced than May, when offers were double those of bids. June posted 130 bids against 132 offers, effectively a 1:1, for 37 trades. Hotei was the clear lead buyer (18 trades) while Dare was again the dominant seller (27 trades), extending its net-short directional bias into the Jet complex as well as Gasoil.

Physical

The physical window saw 66 offers and 60 bids, converting into 4 trades. Liquidity on the sell side was concentrated almost entirely in Gunvor, who placed 44 of the 66 offers (Ampol 11 and BP 7 were the only other notable sellers). Vitol led the bids with 26, followed by Trafigura and BP at 14 apiece.

Bid premiums ran from MOPS flat to +6.00, with offers sitting +1.00 to +5.00, a tighter, more constructive spread than the wide gaps often seen. All 4 trades printed in the final week (June 23–24): Gunvor sold three (to Shell and Glencore) and Ampol one (to Unipec), clearing around the +1.0 to +1.5 level.

Physical Jet stayed heavily offer-skewed at roughly 3.2:1 (42 offers to 13 bids), though less lopsided than May's 6:1, indicating a growth in demand for the physical cargo. Two trades were done, both early in the month (June 5 and 8), with Ampol selling to Vitol and BP at +1.50.

Price Action

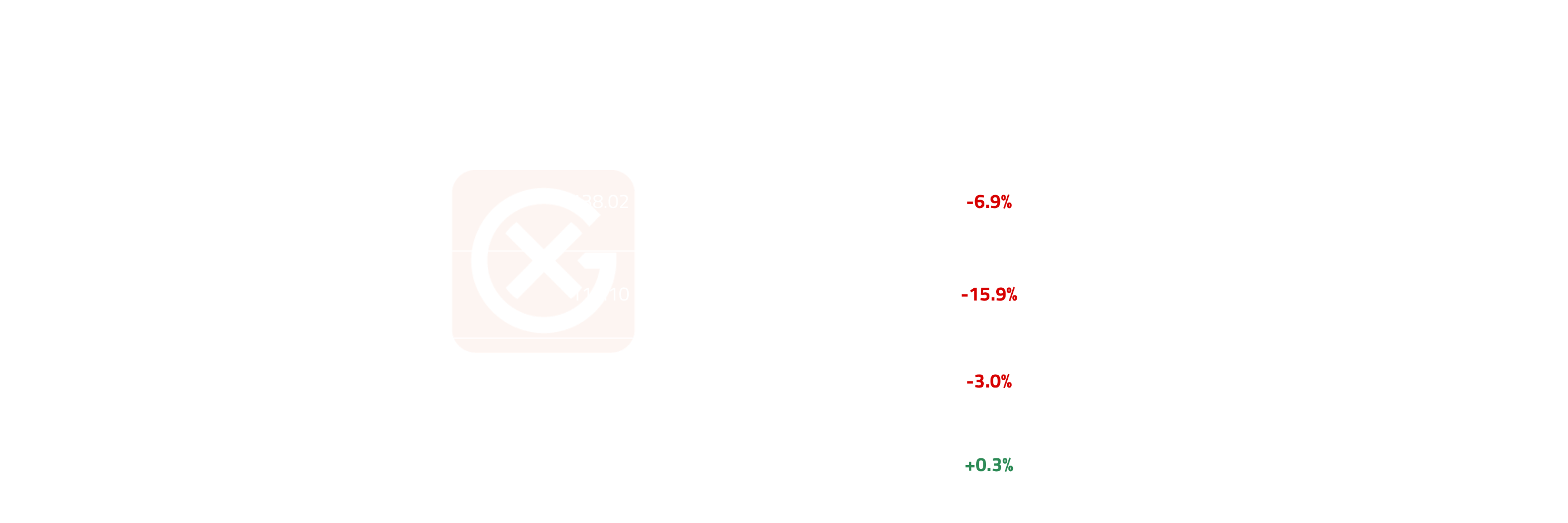

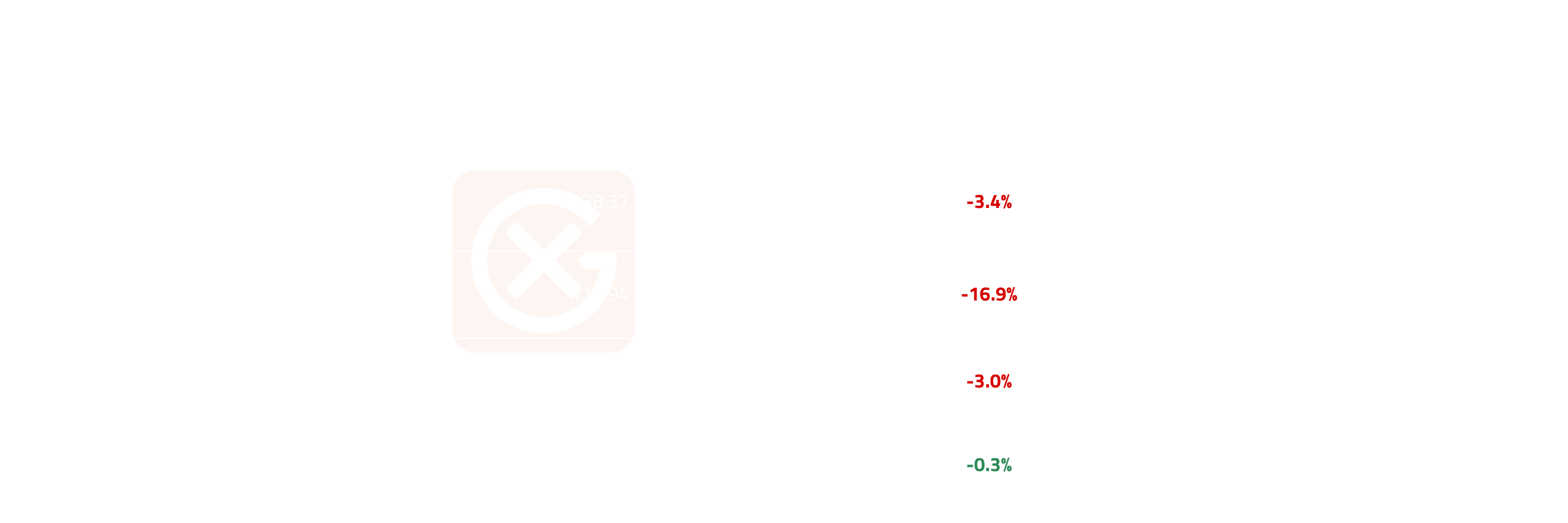

For the month of June, Singapore middle distillates further extended the decline in flat prices seen in May, with Jet having a monthly average of $125.40/bbl vs May's $151.71/bbl (-17.3% MoM) and gasoil averaging $126.98/bbl (-18.3% MoM).

Jet opened $138.05/bbl, closed $111.13/bbl while gasoil opened $146.29/bbl, closed $112.93/bbl. Gasoil fell harder open-close in the month of June (-22.8% vs Jet -19.5%).

Gasoil 10ppm Singapore FOB Cargoes

Jet Fuel Singapore FOB Cargoes

Cross-Market Dynamics

Though cracks to Dubai may have slightly fallen across the month of June, they remain firmly above the levels seen pre US-Iran war – signaling the persistence of supply risk premiums and the Strait of Hormuz’s vital role in middle distillate flows.

M1 cracks held roughly flat within June (Jet $45.42 to $42.78, Gasoil $46.17 to $44.42) while flat price fell ~20%. M1 cracks fell $5-6/bbl, a modest dip in comparison to the ~$26/bbl drop in flat prices. A stable crack in tandem with falling flat prices provides a clear indication that price movements are primarily crude led and of the market’s skepticism on immediate supply relief for gasoil and jet.

Front month regrade initially rose to peaks of $1.31 in the first half of the month but concluded at -$1.64 from the opening of -$0.76. Initial spikes in favor of jet may signal a pickup in demand as summer travel season approaches its peak, a shift from the suppressed demand seen earlier in the year from high jet fuel prices and airline cancellations though it quickly faded towards the end of June. Refineries globally have also capitalized on the earlier spikes in prices for jet by maximizing jet yields for production while the same high prices dampened travel demand. This would have left jet more well supplied in comparison to gasoil, reversing regrade levels to favor gasoil.

Cross-Regional Dynamics

Front month comparisons between NWE Jet and Singapore indicated Europe’s strength over Asia throughout from -$14.10 to -$10.52/bbl (June avg -$10.13). Arbitrage flows saw physical barrels from India depart towards the African continent with quantities received in the months of April, May and June almost double of the previous 12- and 24-month seasonal norms, according to data from analytics company Vortexa. The uptick in Indian flows to Africa instead of Europe, could be related curtailment of crude exports through the Strait of Hormuz, limiting the amount of ‘European friendly-refined products’ India can ship to the West, given the European Union’s sanctions on Russian-origin refined products.

Los Angeles Jet (USWC) held its premium over Singapore Jet (+$19.92 to +$19.28, monthly avg +$15.43), leaving arbitrage opportunities open for jet shipments between Northeast Asia to the structurally short USWC.

East-West gasoil widened modestly (open-close +$6.98 to +$8.53/bbl, monthly avg +$7.01) and points firmly eastward.

Curve Structure

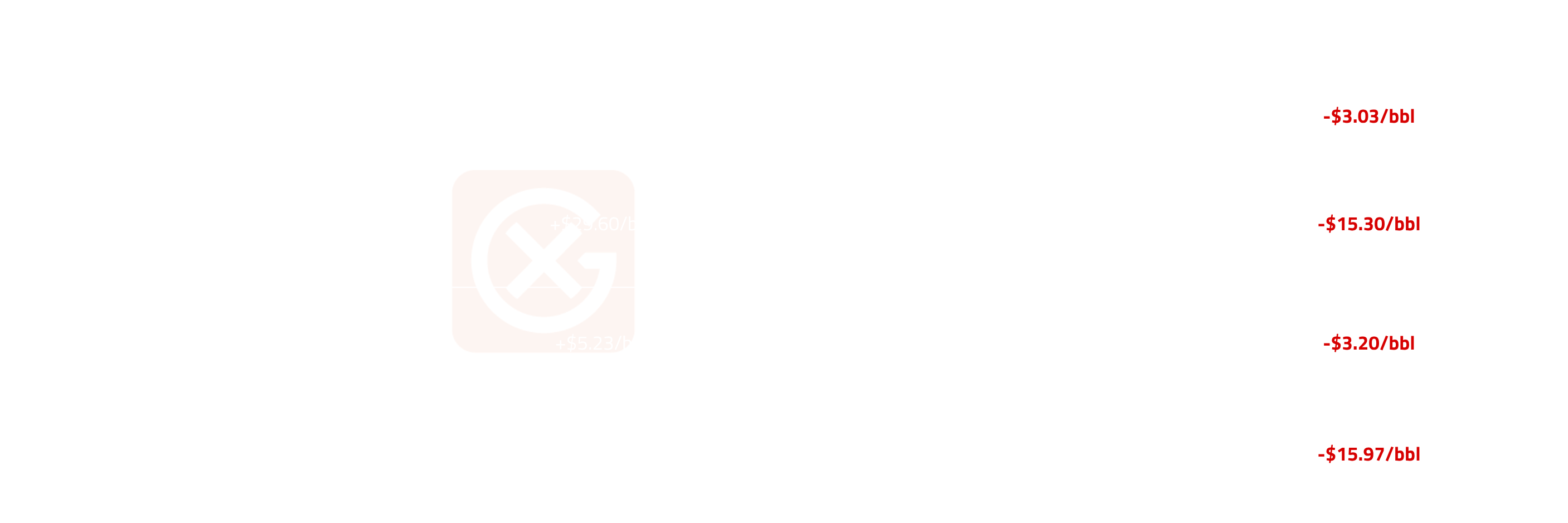

Near term curve structures flattened significantly from backwardation in May for both jet and gasoil as consensus converge upon temporary relief from the US-Iran war and a reduced risk premium in the prompt. An almost flat structure for M1 and M2 was observed by the end of June as the M1-M2 spread for gasoil and jet more than halved from its opening values of $5.23/bbl and $4.25/bbl respectively at the start of June to $1.23/bbl and $2.03/bbl on month close. The remaining tenors have flattened out in the same manner albeit to a lesser extent, remaining firmly backdated with no significant divergence between the two products.

Gradual build up for both US and Singapore stock inventories (2.8% increase in US distillates stocks from the start of June to the week of 19 June and a 16.7% increase for Singapore from the start of the month to the week of 24 June) were observed and may indicate stabilizing supply and also contributed to a more bearish outlook from the market.

Price Volatility

- June Coefficient of Variation (CV) rose to 11.77% (Jet) and 12.19% (Gasoil) from May's 7.55% / 5.82%, a second volatility pickup, but below the March conflict-onset peak (17.37% / 19.98%).

- Jet and Gasoil CV converged near 12%, consistent with a common crude driver rather than a grade-specific event.

Something To Watch

- Chinese export quotas for the month of July at 800,000 metric tons, 200,000 more than what was issued for June would indicate stabilization of China’s domestic fuel supply situation. As current export quotas are below historical norms, a future increase in export quotas for months ahead may further alleviate pricing pressure on the middle distillates especially for net importers such as Australia.

- M1-M2 curve structures for jet and gasoil would indicate ease in prompt tightness as the backwardated structures flatten. A flip to contango would prompt storage economics and incentivize storage of the fuel for future selloffs.

- Traditionally, monsoon season in July for India is likely to dampen domestic agricultural and industrial diesel demand, providing more diesel barrels for export. However, the El Nino weather event could defer or cause the monsoon to have a disproportionate effect on the agricultural industry.

- Russia’s response to Ukraine’s strikes, with local media reports that the country may resort to importing fuel amidst disruption to refining capacity. With Africa, Turkey and Brazil being the largest buyers, how Russia responds on diesel barrels will affect the global diesel balance and potentially lift diesel prices.

Note: All figures, prices and market activity referenced in this report are based on the period 2-30 June 2026.