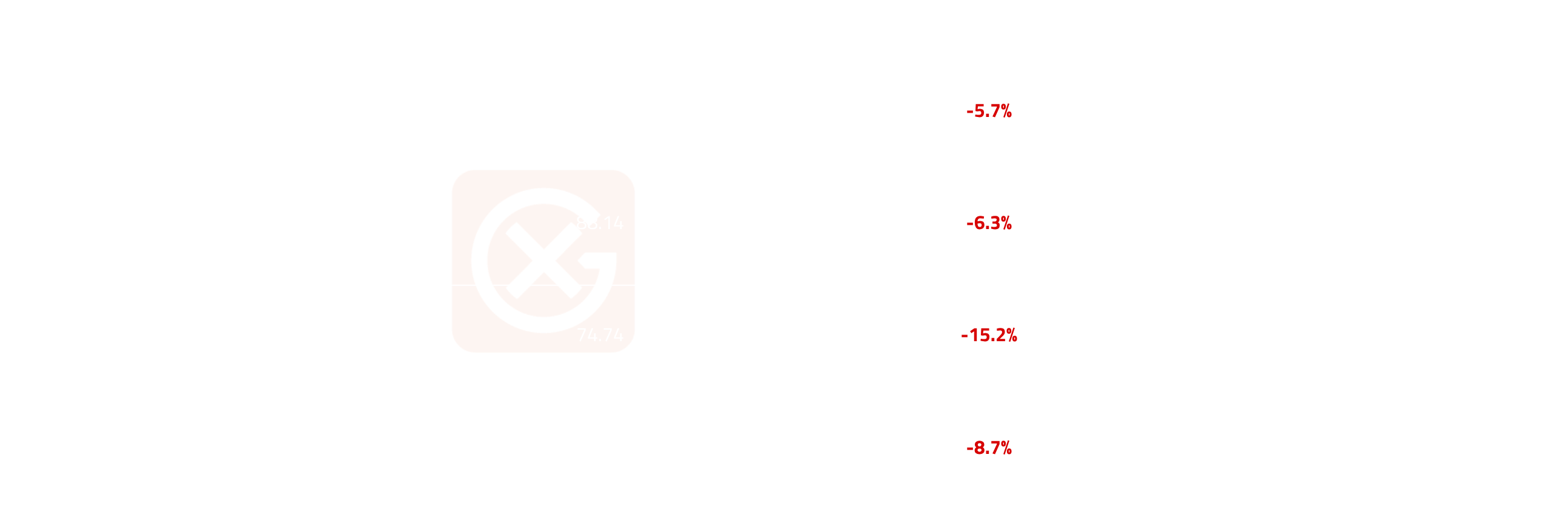

Outright Dubai crude prices fell below $100/bbl for the first time since the onset of the conflict, declining $23.89/bbl MoM to $79.40/bbl on average and closing at $68.29/bbl on 30 June, as the US-Iran Memorandum of Understanding (MoU) signed on 17 June triggered the steepest weekly sell-off of the year (-15.2% WoW). Both Dubai and IFAD Murban M1-M3 structures flipped into contango as improved Gulf flows combined with depressed Chinese refinery runs (-20% on year). Brent-Dubai EFS narrowed to $3.05/bbl on the last trading day as Asian refiners rotated back toward sour grades coming out of the Strait of Hormuz.

Market Activity

- 58 total partials traded for Aug-26 loading with no convergence observed; absence of convergence for a second consecutive month may reflect reluctance by participants to commit to physical settlement amid uncertainty over basket of deliverable grades in the Dubai window and ongoing legal disputes between parties.

- Shell was the dominant seller with 28 partials (48% of total offer side), selling heavily to Vitol (15) and Trafigura (6); Vitol (21) and Trafigura (19) were the dominant buyers, together absorbing 40 of 58 partials (69%).

- Shell’s selling activity could be indicative of loosening supply amid reopening of the Strait of Hormuz.

- Trading houses were building long Dubai positions, supported by their view of an uptick in Chinese demand for crude amid lower crude prices.

- Phillips 66 (5 sells, 5 buys) and BP (5 sells, 2 buys) were two-way for a third consecutive month, consistent with integrated major portfolio rebalancing rather than directional positioning.

Price Action

- Open $92.80/bbl (2 June), close $68.29/bbl (30 June), monthly avg $79.40/bbl vs May's $103.29/bbl (-$23.89/bbl MoM, -23.1%; close nearly flat YoY at -$0.47/bbl vs June 2025's $68.76/bbl, retracing the war risk premium.

- Monthly high $97.41/bbl on 3 June; monthly low $64.39/bbl on 25 June; intra-month range $33.02/bbl was more than 3x May's $10.69/bbl, the widest since March's $88.95/bbl disruption-driven range.

- W3 was the breakout sell-off week at -15.2% WoW as the MoU was signed on 17 June; the muted W4 close of $68.02/bbl avg (-8.7% WoW) despite Iran's strait re-closure on 20 June and US strikes on 26 June confirms de-escalation is the market's base case.

Cross-Market Dynamics

- GME Oman Futures (GX0000027) averaged $79.09/bbl vs Dubai's $79.40/bbl, a narrow -$0.31/bbl discount, narrower than May's -$1.29/bbl; closed at $65.20/bbl (-$3.09/bbl vs Dubai) as benchmarks normalised closer together amid increasing crude flow from the Strait of Hormuz.

- IFAD Murban Futures (GX0000643) averaged $80.01/bbl, a slight +$0.61/bbl premium to Dubai vs May's -$1.28/bbl discount; closed at $68.76/bbl (+$0.47/bbl vs Dubai), a sharp reversal of May's -$11.35/bbl as medium sour crude availability from the Strait of Hormuz returned, as evidenced in QatarEnergy and ADNOC sell tenders.

- Murban's M1-M3 structure flipped into contango from 15 June, averaging -$1.17/bbl over 15-26 June.

- ADNOC tenders awarded approximately 60mn bbl or more of Upper Zakum, Das Blend, and Umm Lulu for June-August loading, confirming Asian refiner demand for sour Gulf grades is returning as Hormuz accessibility improved.

Cross-Regional Dynamics

- Brent-Dubai EFS (GX0000585) averaged $7.21/bbl in June vs May's $11.14/bbl; opened at $8.04/bbl and narrowed to $3.05/bbl by 30 June, the tightest close since the conflict began, as markets priced near-full convergence back toward normalized Middle East Gulf-Atlantic basin trade economics.

- The EFS compression reversed the May dynamic; improved Hormuz accessibility reduced urgency of Atlantic Basin sourcing, enabling Asian refiners to rotate back toward sour Gulf grades as evidenced by ADNOC tender awards and renewed interest in Upper Zakum, Das Blend, and Al Shaheen.

- Dubai flat price upside remains capped by Atlantic competition while the EFS stays below $5/bbl; however, the directional trend is now toward stabilization if Hormuz transit normalizes through the MoU's 60-day window.

Curve Structure

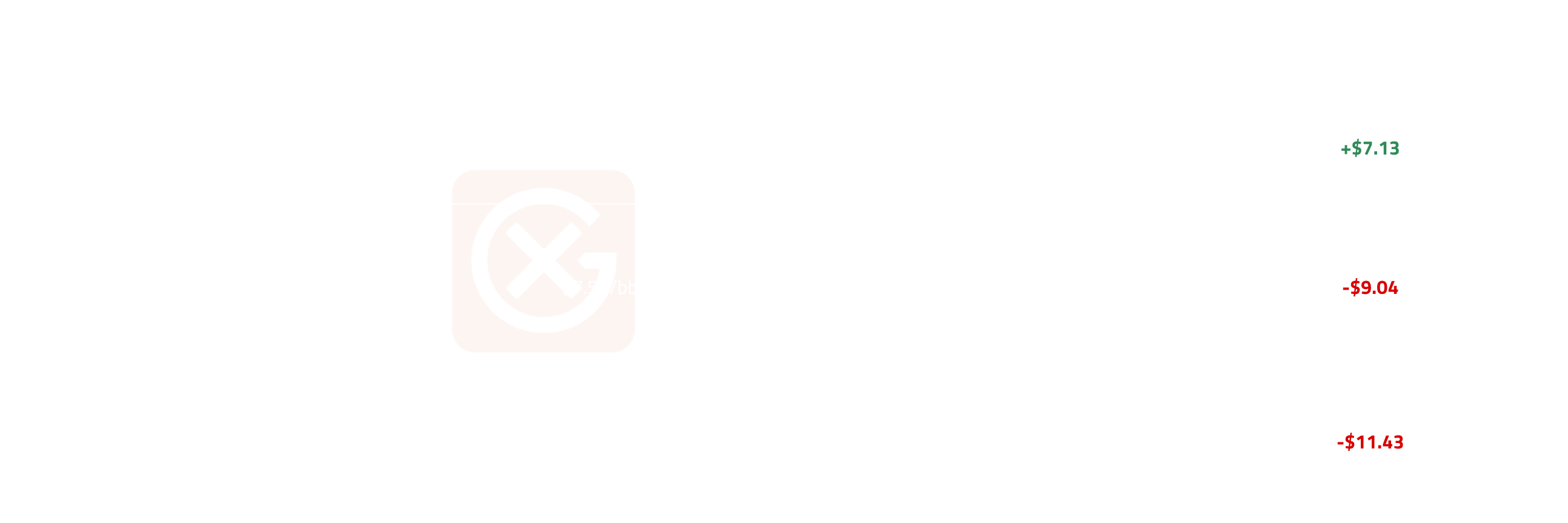

- M1-M2 (GX0000586) opened $3.57/bbl and closed $10.70/bbl (+$7.13/bbl); the widening reflects acute day-to-day uncertainty at the very prompt as Iran's partial closures and US strikes kept near-term transit risk elevated.

- M1-M6 opened $7.54/bbl and closed -$1.50/bbl; M1-M12 opened $10.73/bbl and closed -$0.70/bbl; both flipping into contango confirming the market has priced out the Gulf risk premium in the medium and long term, pricing gradual supply normalization as the base case.

- The divergence between a widening M1-M2 and negative M1-M6 and M1-M12 is structurally significant: the curve is pricing simultaneously prompt uncertainty and back-end resolution, a configuration that unwinds sharply in either direction depending on the MoU durability in July.

Price Volatility

- June Coefficient of Variation (CV) of 13.87% is roughly 4x May's 3.50% and the highest since March's 21.72% peak; unlike March's disruption-driven spike, June's volatility was resolution-driven, a $33.02/bbl intra-month range generated by the US-Iran MoU signing and optimism in future peace negotiations rather than a new supply shock.

- Risk models recalibrated to the 3-7% CV range seen in April-May underestimated de-escalation event risk; until Hormuz transit data confirms durable normalization, elevated CV should remain the baseline for position sizing.

Something to Watch

- MoU durability is the binary catalyst for July; watch for further ADNOC and QatarEnergy spot tenders as the clearest indicator of returning Asian refiner demand for sour Gulf grades.

- Return of liquidity in the Dubai partials window would signal confidence by market participants to return to normal trading patterns. Apparent acceptance by ADNOC to switch official selling prices for Upper Zakum, Das, and Umm Lulu to Dubai basis from the current IFAD Murban basis may support Dubai window liquidity.

- Dubai M1-M3 averaged -$0.97/bbl over 23-30 June; a snap back to backwardation would be the next physical signal of Chinese demand recovery.

Note: All figures, prices and market activity referenced in this report are based on the period 1–30 June 2026.