HSFO 3.5% FOB ARA Barges fell 22% on the month and VLSFO 0.5% fell 17%, but this was a crude selloff rather than a fuel oil story: Dated Brent dropped 28%, from roughly $100 to $71/bbl, as Strait of Hormuz transits reopened on US-Iran de-escalation.

The key metric here is the Hi-Lo spread, which blew out from $60 to $128/mt over the month and averaged $90/mt against $70/mt in May, as VLSFO held firm while returning heavy-sour supply dragged HSFO lower.

That HSFO's crack to Brent barely moved, holding near -$9/bbl as in May, confirms the point, since it shows HSFO simply followed crude down rather than weakening on its own. The forward curve tells the same story, with HSFO's backwardation collapsing into the default mild contango (M1-M2 from +$16 to -$1/mt) while VLSFO kept its shape at +$20/mt, and the participant data echoes it, as the HSFO buy/sell ratio normalized from 4.71 to 1.51 on the return of sell-side offers.

HSFO was also its most volatile all year, with a June CV of 12.6% that sat above the March dislocation and nearly double VLSFO's 6.8%.

The path from here is binary: if Gulf supply keeps normalizing, HSFO's contango holds and the Hi-Lo stays wide, whereas a fresh Hormuz disruption would re-tighten HSFO and pull backwardation back.

Market Activity

HSFO sell-side returned as offers nearly tripled and the buy/sell ratio normalized from 4.71 to 1.51; Aramco Trading's HSFO selling jumped ~7x, the participant-side print of heavy-sour supply coming back.

- In the HSFO barge window, June ran 284 bids against 188 offers for a 1.51 buy/sell ratio on 76 trades, against May's far more lopsided 363 bids and just 77 offers (a 4.71 ratio on 96 trades), with the ratio normalizing because offers nearly tripled as sellers returned to a window that had been acutely bid-dominated in May.

- That return of sell-side liquidity is the participant-side confirmation of the curve and crack story, with producers and intermediaries offering barrels freely again as prompt tightness eased rather than holding them back.

- Producer supply showed up directly, as Aramco Trading sold over 10 HSFO trades in June against just 2 in May to rank second only to Vitol, so heavy-sour barrels returning to the Gulf export pool surfaced as producer offers in the ARA window.

- Vitol stayed the top HSFO seller but halved its pace in June, so intermediary offer volume slowed even as total offers rose, with producer and reseller sellers such as Aramco and Orim filling the gap.

- Shell Trading led HSFO buyers in both months, with bunker reseller United Bunkers in the top three, consistent with delivered-stem coverage on the buy side.

- The VLSFO barge window was far steadier, running 297 bids against 184 offers for a 1.61 ratio on 88 trades, close to May's 1.83 ratio on 101 trades, in keeping with VLSFO's intact curve and held premium.

- The buy side changed hands, as bp Netherlands, the dominant VLSFO buyer in May, flipped to the sell side in June and dropped out of the top buyers, a switch that reads as length reduction, monetizing inventory while VLSFO held firm.

- Glencore stepped in as the top VLSFO buyer, while ExxonMobil worked both sides of the window, intermediary positioning rather than directional flow.

Price Action

HSFO fell 22% and VLSFO 17% as Brent's 28% slide dragged the complex; Week 24 was the breakout-down week.

- HSFO averaged $488/mt in June, down 22% from May's $626/mt and the steepest monthly drop in the 13-month series, opening at $581/mt and closing at $408.25/mt.

- VLSFO fell less, easing 17% to a $578/mt average as it opened at $640.75/mt and closed at $535.75/mt.

- Both grades are still up year-on-year (HSFO +13%, VLSFO +20%), so while June unwound most of the March disruption premium, it did not break below the pre-disruption base; this was a normalization, not a collapse.

- HSFO's intra-month range widened to $183/mt, half again as wide as May's $119/mt, and a range that wide is itself a regime shift driven by the crude move.

- Both grades fell around 7% in a single 12 June session (HSFO -$38.25/mt, VLSFO -$43.50/mt), the same day Brent dropped sharply, and the fact that they moved together points to crude rather than a fuel-oil-specific event.

- Week 3 (15-19 June) was the breakout-down week as Hormuz transits reopened, with HSFO losing 14% and VLSFO 9%.

- The two grades split late in the month, as VLSFO flattened out near its lows at around 1% a week while HSFO kept sliding (-7%, then -3%), so VLSFO had found a floor while HSFO was still normalizing lower.

Cross-Market Dynamics

Hi-Lo blew out from $60 to $128; a flat HSFO crack shows HSFO only tracked crude.

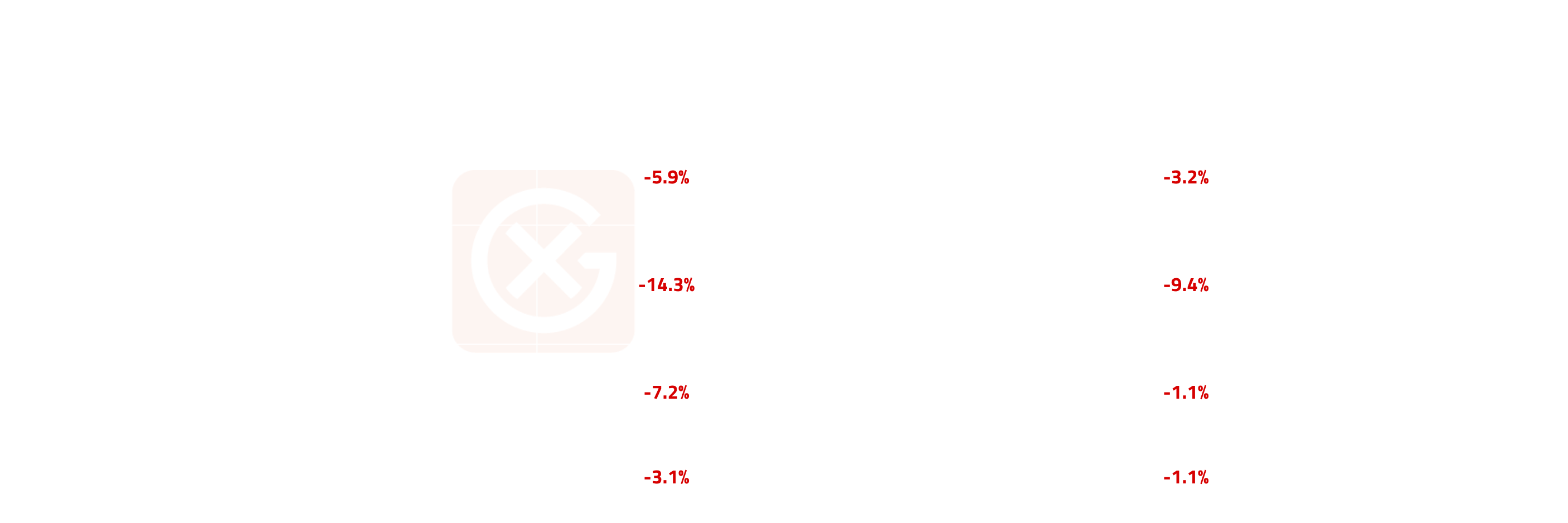

- The Hi-Lo spread (VLSFO minus HSFO) widened from $59.75/mt at the open to $127.50/mt at the close, averaging $89.88/mt for the month against $70.17/mt in May, with the widest print of $128.75/mt on 26 June.

- HSFO's crack to Brent was flat month-on-month, averaging -$9.19/bbl versus -$8.90/bbl in May, and ranging from -$11.54/bbl early on to -$6.61/bbl by 23 June.

- That flat crack is the analytical point, because it shows HSFO fell in step with crude rather than weakening against it, which makes the Hi-Lo blowout a case of VLSFO holding its premium as heavy-sour supply returned, the inverse of a tightening signal rather than an HSFO squeeze.

- The crack even firmed slightly into month-end, but only because Brent fell faster than HSFO in the final week, a knock-on of the crude slide rather than any residual tightness.

Cross-Regional Dynamics

East/West arbs compressed sharply as the Singapore premium shrank; HSFO E/W collapsed from +$81 to +$25/mt, thinning the eastbound pull, while the VLSFO premium stayed wider.

- The HSFO East/West spread (Singapore 380 minus ARA HSFO) compressed from +$80.70/mt on 2 June to +$24.75/mt by month-end, averaging +$31.91/mt against May's +$54.51/mt, with a high of +$80.76/mt on 4 June and a low of +$1.82/mt on 23 June.

- As the East premium shrank toward marginal levels, the incentive to move ARA HSFO cargoes East weakened, leaving more heavy-sour supply in ARA and compounding the prompt softness already coming from the supply return.

- The VLSFO East/West spread (Singapore 0.5% minus ARA VLSFO) also compressed, from +$133.16/mt to +$53.62/mt for a June average of +$77.44/mt against May's +$99.10/mt, but it stayed well wider than HSFO throughout, bottoming at +$28.99/mt on 25 June.

- That wider, more durable premium kept the eastbound VLSFO arb comfortably open while HSFO's narrowed toward marginal, and with Singapore VLSFO holding its premium just as ARA VLSFO did, the low-sulphur strength looks like a global feature rather than an ARA quirk.

- Both spreads peaked on the same day, 4 June, and then compressed in step with the crude-led selloff, so the two regions repriced together rather than diverging; this is a complex-wide easing showing up at both ends, not an East-versus-West dislocation.

Curve Structure

HSFO bear steepening; backwardation collapsed across the whole curve (M1-M2 +$16 to -$1, M1-M24 +$112 to +$22) while VLSFO held its shape to M24.

- HSFO showed bear steepening, with the front falling faster than the back (M1 down $192/mt against M24 down $102/mt) and its backwardation collapsing across the whole curve, as M1-M2 tipped from +$16/mt into -$1/mt contango, M1-M3 went flat, and M1-M24 fell from +$112/mt to +$22/mt.

- Crucially the back end repriced too, not just the prompt, with M12 down $111/mt and M24 down $102/mt, so the disruption premium came out of the entire curve, which marks genuine normalization rather than a prompt-only unwind.

- Mild contango is this curve's normal state, so the move is best read as the backwardation signal fading as heavy-sour barrels returned rather than a new structural shift, and a settle into sustained contango would confirm the prompt tightness has fully cleared.

- VLSFO kept its shape, holding M1-M2 at +$20/mt all month and staying backwardated all the way to M24 (+$61/mt at the close) while narrowing only modestly further out, a sign that near-term VLSFO demand stayed supported even as HSFO normalized.

- This split between the two curves is the structural counterpart to the Hi-Lo blowout, with HSFO losing its backwardation across the curve while VLSFO kept its.

Price Volatility

HSFO June CV of 12.6% was the highest in H1 2026, above the March dislocation; VLSFO at 6.8% shows the move was HSFO-specific.

- HSFO's June CV of 12.6% was its highest reading of the year, above even the March dislocation at 10.0%, reflecting the $183/mt range as the front collapsed.

- VLSFO was far calmer at 6.8%, below its own March reading, and the gap between the two grades (12.6% versus 6.8%) shows the volatility sat almost entirely in HSFO.

- Hedging models tuned to HSFO's calm 5-6% range in April and May are understating current risk by roughly 2.5x, so until supply normalization is confirmed, elevated HSFO volatility should be treated as the planning baseline.

Something To Watch

HSFO M1-M2 contango as the normalization-completion signal:

- Observation: M1-M2 flipped from +$16/mt backwardation on 1 June to -$1/mt contango on 29 June, with M1-M3 at zero.

- Why it matters: a settle into sustained mild contango (the default) would confirm the disruption-era tightness has fully cleared, while a re-flip into backwardation would flag renewed Gulf supply disruption before it shows in flat price.

- What to monitor: the weekly M1-M2 close on ICE 3.5% Barges, Persian Gulf export and Hormuz transit rates and Saudi and wider Gulf loadings.

Note: All figures, prices and market activity referenced in this report are based on the period 1–29 June 2026.