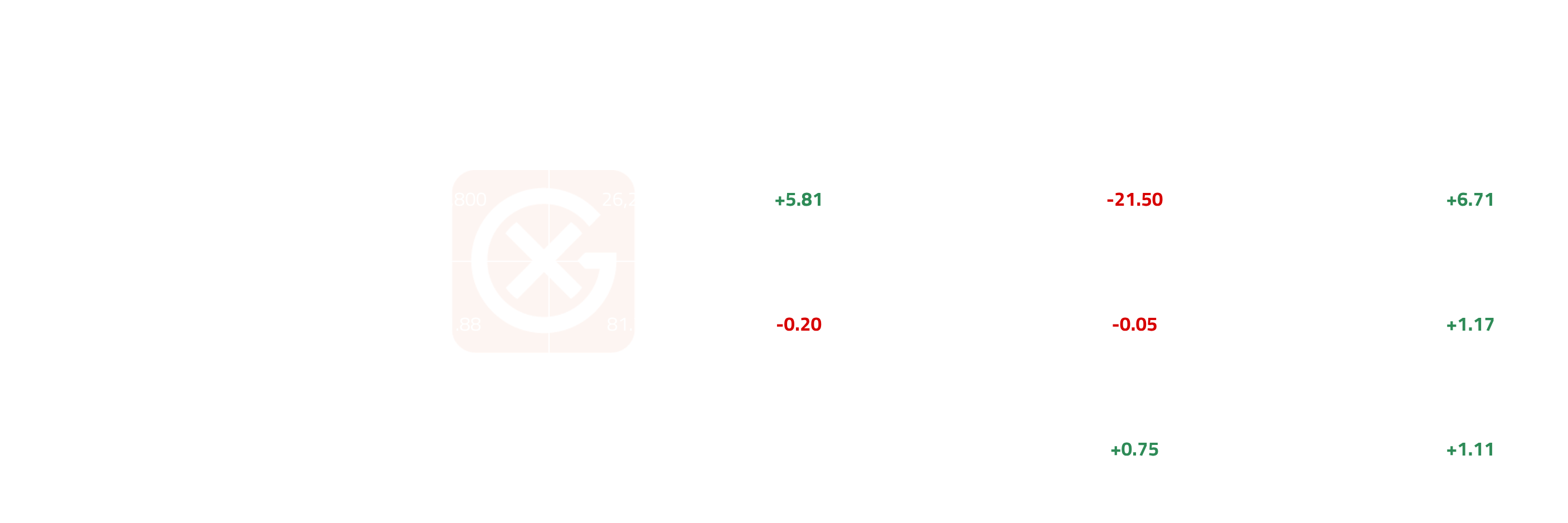

Global compliance carbon markets were mixed in June 2026. In North America, California LCFS and CCA strengthened on tighter program rules, while Washington allowances fell sharply as the market priced in an expected drop in prices following the signing of a linkage agreement with California and Québec. In Europe, both EUA and UKA rose, with UKA outperforming as markets positioned ahead of the expected EU-UK linkage confirmation at the 13 July summit. In Asia-Pacific, Korea KAU was the most volatile mover in the complex, spiking 22% intra-month before reversing to close 2.3% below its open as the market digested the new Phase 4 stability reserve; China CEA and New Zealand NZU were comparatively stable, both posting modest upward drift. The week of 13–15 July is the key near-term event risk, with EU-UK linkage and the EU ETS reform proposal both due.

Market Activity

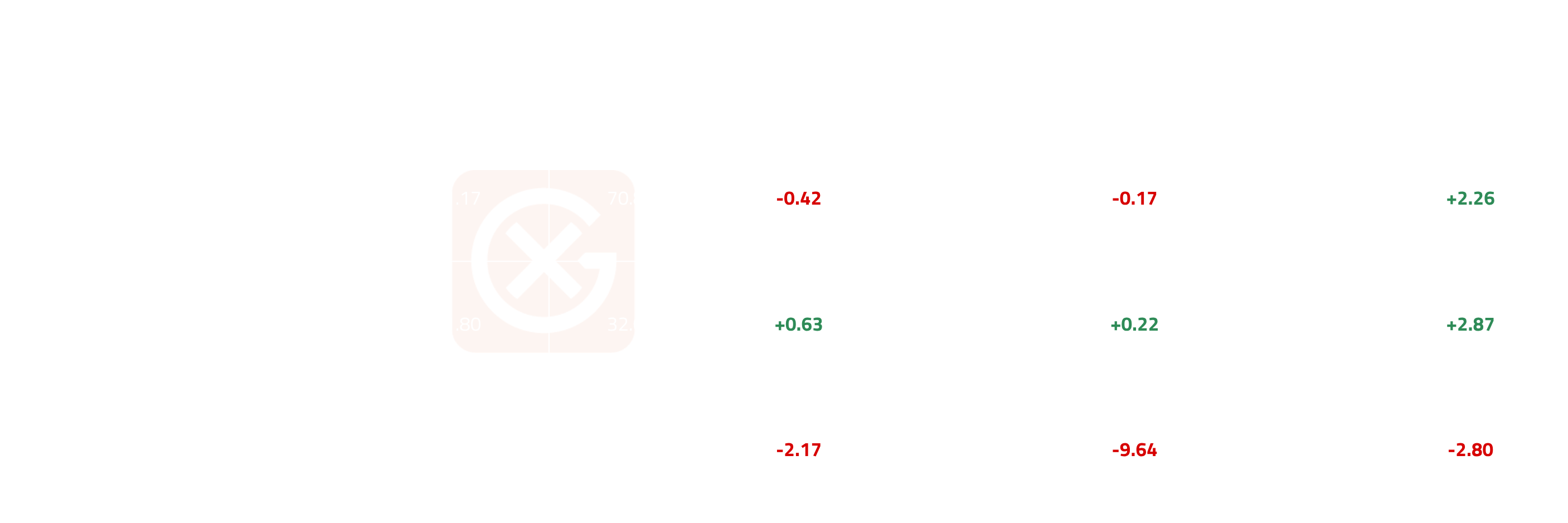

North America

- LCFS (California and Oregon) is supported by structurally tighter CI targets from the 2024 Amendments combined with a slump in renewable diesel supply, which has pushed deficits above credits for the first time in years.

- CCA is supported by California's extension of its cap-and-invest program through 2045 and an accelerating cap reduction trajectory under CARB's 2026 tightening plan.

- WCA is falling as the market prices in convergence toward the lower California-Québec joint allowance price ahead of the Washington-California-Québec linkage agreement signed in June 2026.

Europe

- EUA is supported by confirmed supply tightening: the scheduled 27 million allowance 2026 cap rebasing, plus the REPowerEU revenue target being reached on 22 June, which cuts per-auction volume from 3.2mn to 2.8mn allowances through August.

- UKA and the EUA/UKA ratio are pricing in an EU-UK ETS linkage expected to be confirmed at a 13 July summit; the spread has already narrowed to its tightest level since early February on anticipation.

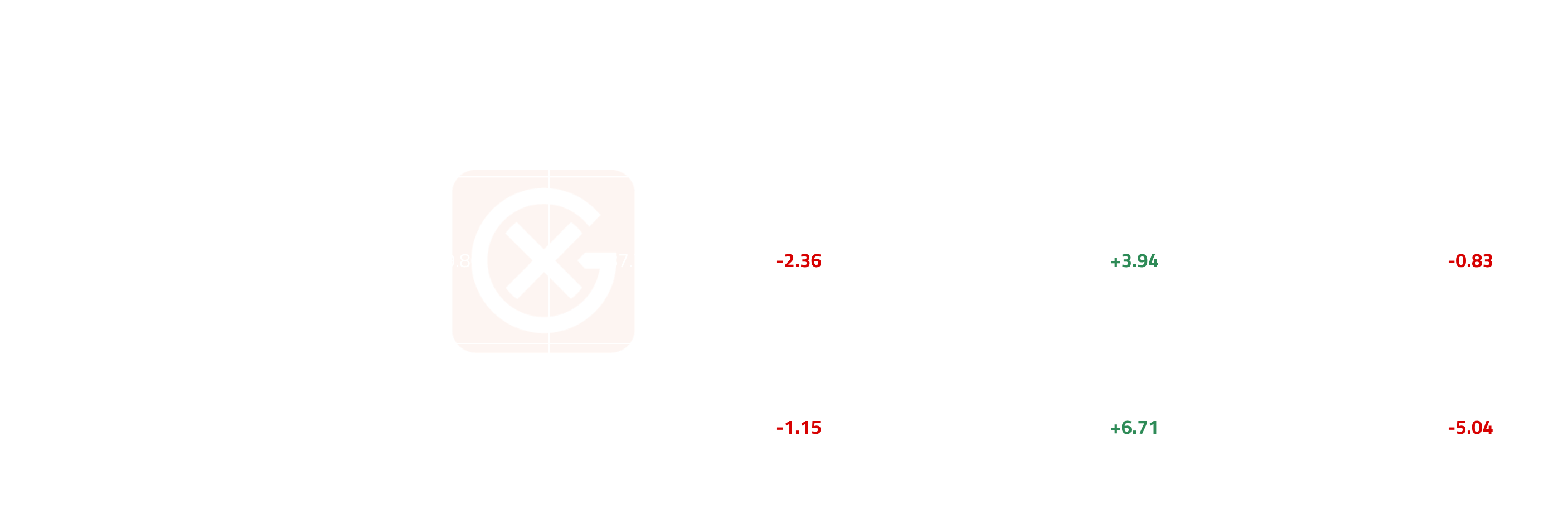

Asia-Pacific

- New Zealand NZU drifted modestly higher through June, closing at NZD 55.75 (+1.9% MoM); the move is consistent with forecast unit scarcity ahead of the government's auction volume consultation (see Something to Watch).

- Korea KAU traded with significant two-way volatility in June as the market digested the newly introduced quantity-based market stability reserve under Phase 4 (2026-2030); spot opened the month at KRW 23,500, spiked to a monthly high of KRW 28,800 (8-Jun) on continued positioning, then reversed sharply to a monthly low of KRW 19,600 (17-Jun), a 32% collapse, before recovering to close at KRW 22,950 (29-Jun).

- China CEA held a narrow CNY 80.77-83.12 range through June (monthly average CNY 82.04), supported by the 2025 expansion of the national ETS to cover steel, cement, and aluminium smelting, lifting coverage from 40% to 60% of China's GHG emissions, with allocation for these sectors shifting to intensity-based benchmarking (MEE).

- Japan J-Credit Energy Efficiency opened June at JPY 4,800, closed at JPY 4,900 (+2.1% open-to-close, +2.0% MoM average); the modest recovery follows May's softening and remains within a thinly traded, infrequently assessed market.

Price Action

North America

Europe

Asia-Pacific

Something To Watch

- The EU and UK are expected to formally confirm ETS linkage at the 13 July summit, with the EU ETS reform proposal also due on 15 July, making that week the most important for European carbon pricing this year.

Note: All figures, prices and market activity referenced in this report are based on the period 1 to 30 June 2026