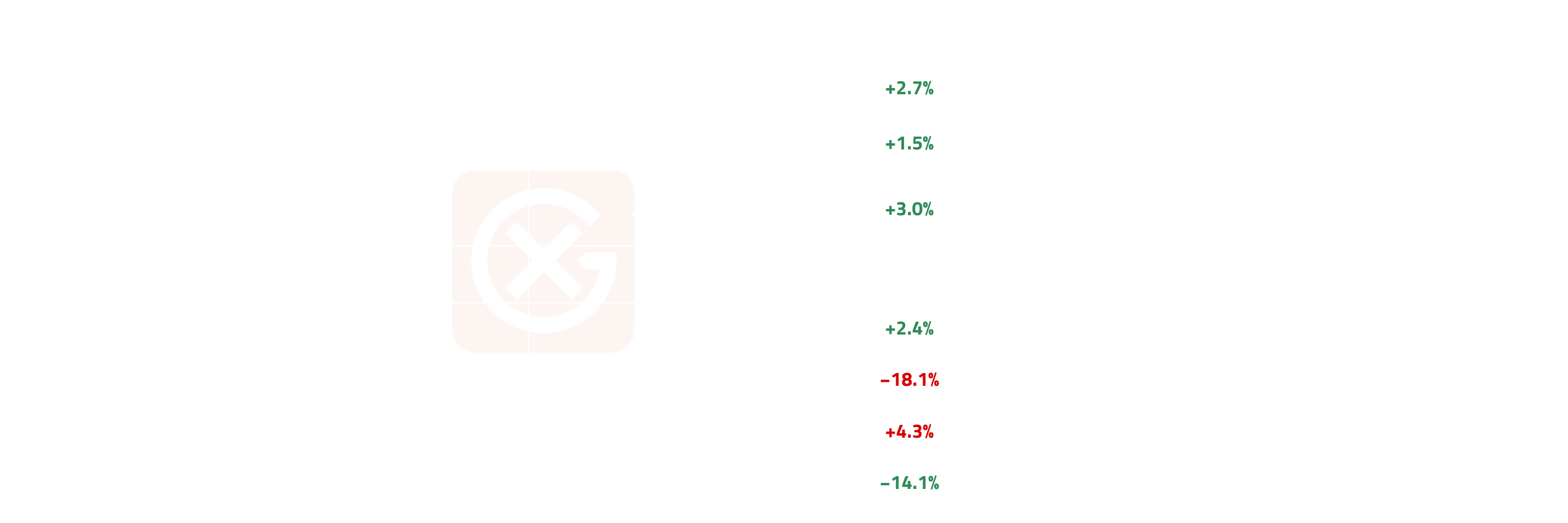

The voluntary carbon complex split along the removal-versus-avoidance line in June as the SBTi published its final Corporate Net-Zero Standard V2.0 on 11 June, mandating durable-removal purchases for large companies from 2035 while keeping avoidance credits out of target accounting. Removal benchmarks stepped up one session ahead of publication and held: NBS Removal rose to $21.10/mt (+3.0% MoM, +19.0% YoY) and Tech Removal to $22.45/mt (+2.4% MoM, +16.9% YoY), widening the removal-over-avoidance premium from $13.50 to $14.40/mt. NBS Avoidance stayed pinned to its assessed floor at $6.70/mt all month (CV 0%, −20.5% YoY), with no demand pull to lift it. CCP Current firmed +2.7% MoM but faded within the month to a $5.45/mt close as relative-value demand concentrated in pure removals rather than the broad CCP basket; its +72.5% YoY integrity premium is intact. The clear outlier was CORSIA: CEEU fell −14.1% MoM to a $9.40/mt close (−29% since its April launch) as rising host-country authorizations and IATA-coordinated procurement unlocked eligible supply ahead of a Phase 1 deadline not due until January 2028. Volatility compressed across the complex, leaving the spreads, not flat price, as the month’s signal: the widening removal premium and the CEEU grind lower are the positions to watch into the 2035 removal ramp and the 2028 CORSIA deadline.

Price Action

All indices USD/mt, GX-assessed spot (current vintages). CEEU = CORSIA Eligible Emissions Units (Europe). CEEU series launched April 2026; no YoY available.

Price Volatility

Coefficient of variation (standard deviation / mean), monthly. June shows broad compression: five of eight indices at or near 0% CV; only CCP (4.32%) and NBS Removal (2.09%) carried meaningful dispersion. CEEU history begins April 2026.

Market Drives

- SBTi Net-Zero Standard V2.0 validated structural removal demand. The final V2.0 (published 11 June) requires Category A companies to buy carbon removals from 2035, starting at 1% of footprint and rising to 100% by their net-zero year, of which at least 10% must be durable in 2035 rising to 100%; credits remain barred from Scope 1/2/3 target accounting. The removal complex stepped up on 10 June, one session ahead of publication: NBS Removal +$0.90 to $21.10 and Tech Removal +$0.50 to $22.45, both holding to month-end. Mechanism: a fixed forward demand schedule for nature and durable removals pulls current-vintage removal benchmarks higher.

- Avoidance excluded from target accounting kept NBS Avoidance on its floor. With V2.0 reaffirming that avoidance credits cannot count toward Scope 1/2/3 targets, and ICVCM CCP filtering continuing to price sub-$15 nature avoidance out of buyer-grade portfolios, NBS Avoidance held flat at $6.70 all month (CV 0%, fourth flat reading in six months), −20.5% YoY. Mechanism: with no compliance or neutralization demand pull, the benchmark sits on its assessed floor.

- Intra-integrity rotation: the broad CCP basket gave back late-May strength. CCP Current opened June at $5.95, held through Week 2, then faded to a $5.45 close (single −$0.50 on 18 June) even as removal indices firmed. Mechanism: post-V2.0, relative-value demand concentrated in pure-removal benchmarks rather than the broad CCP basket, which spans avoidance and reduction methodologies. The +72.5% YoY CCP integrity premium is structurally intact; June was a give-back, not a reversal.

- CEEU fell as eligible-supply unlock outpaced not-yet-urgent Phase 1 demand. CORSIA’s binding constraint is host-country Letters of Authorization, not headline demand (Phase 1 need 146–236 million units). LoA-issuing host countries rose from roughly seven in early 2026 to about ten by April, and IATA coordinated supply via an airlines-only EEU Procurement Event (Guyana, Mercuria, Xpansiv) and the Supporting Alliance for CORSIA EEU Supply, with the IATA AGM held 6–8 June. With Phase 1 cancellation not due until January 2028, incremental eligible supply is arriving ahead of urgent buying. Mechanism: supply unlock outpacing near-term demand ground CEEU from its ~$13.20 April launch to a $9.40 close (−14.1% MoM) on a low 2.11% CV, an orderly decline rather than a volatility event.

- BeZero AA’s −18.1% MoM is a base effect, not fresh weakness. AA held flat at $7.80 throughout June (its May closing level, CV 0%); the average decline reflects May’s mid-month spike to a series-high $9.52 average fading, not June selling. AA − A narrowed slightly ($3.45 to $3.35) as A firmed +4.3% MoM.

Something To Watch

- Removal premium as the SBTi V2.0 transmission gauge

- Observation: NBS Removal − NBS Avoidance widened to $14.40 (close); Tech Removal − NBS Removal narrowed to $1.35.

- Why it matters: V2.0 channels mandated neutralization demand into removals; a sustained widening of the removal premium confirms demand pull building ahead of the 2035 ramp, while the narrowing tech-over-nature removal gap signals buyers treating nature removals as the lower-cost durable entry point.

- What to monitor: weekly NBS Removal − NBS Avoidance spread; publication of the SBTi Claims System (detailed claim conditions still pending); GHG Protocol Land Sector and Removals Standard uptake.

- NBS Avoidance floor integrity

- Observation: NBS Avoidance flat at $6.70, CV 0%, fourth flat month in six.

- Why it matters: the floor holds only while no fresh bid emerges; a break below $6.70 would signal avoidance demand erosion accelerating, while an uptick would signal CORSIA or contribution-claim buyers re-entering the low-cost avoidance pool.

- What to monitor: the first non-$6.70 print; ICVCM CCP methodology approvals or rejections affecting avoidance eligibility.

- CEEU supply-demand inflection into the Phase 1 deadline

- Observation: CEEU −14.1% MoM to $9.40, −29% since the April launch, on low CV.

- Why it matters: the orderly decline reflects supply arriving ahead of demand; as the January 2028 cancellation deadline nears, airline buying should compress the issued-versus-eligible gap and can reverse direction, with supply-constrained scenarios cited as pushing prices materially higher.

- What to monitor: monthly LoA-issuing host-country count; ICAO TAB Phase 2 (2027–2029) programme approvals; CEEU weekly direction for the first higher close.

Note: All figures, prices and market activity referenced in this report are based on the period 1 to 30 June 2026.