The Strait of Hormuz closure that choked Middle East diesel and jet exports forced Europe and Asia to pull US barrels, keeping the distillate margin extreme even as June's de-escalation unwound crude faster than product. Flat ULSD NYH fell 13.2% MoM to 341.5 cpg (=$143.4/bbl), but the ULSD-WTI Houston crack gave back only 4.83% MoM, held +119% YoY, and eased just gradually off its March peak ($70 to $61.2). US distillate stocks near 106 million barrels, roughly 12 million (about 10%) below the five-year average (EIA), keep the margin rich and the curve backwardated (M1-M2 +6.3 to +8.6 cpg), while jet weakened against diesel, the jet-ULSD spread deepening to -41.0 cpg.

Market Activity

- Trade data for the NA distillate windows was not included this month.

Price Action

- June's Hormuz de-escalation dragged flat diesel down with crude: NYH averaged 341.5 cpg (=$143.4/bbl), down 13.2% MoM but +49.7% YoY on structurally low Russian export supply.

- Product refused to follow crude all the way, walking 371.4 to 318.0 to 331.8 cpg into a W4-W5 floor; the biggest drop, -19.4 cpg on 04 Jun, was crude-led as the crack fell the same session.

- Midcon unwound more than the coast, Group 3 Magellan (-17.3% MoM) and Badger Chicago (-22.9% MoM) hardest; Gulf-up basis compressed to 8.8 cpg avg (-14.8% MoM), still above the roughly +5 cpg it takes to open the arb.

Cross-Market Dynamics

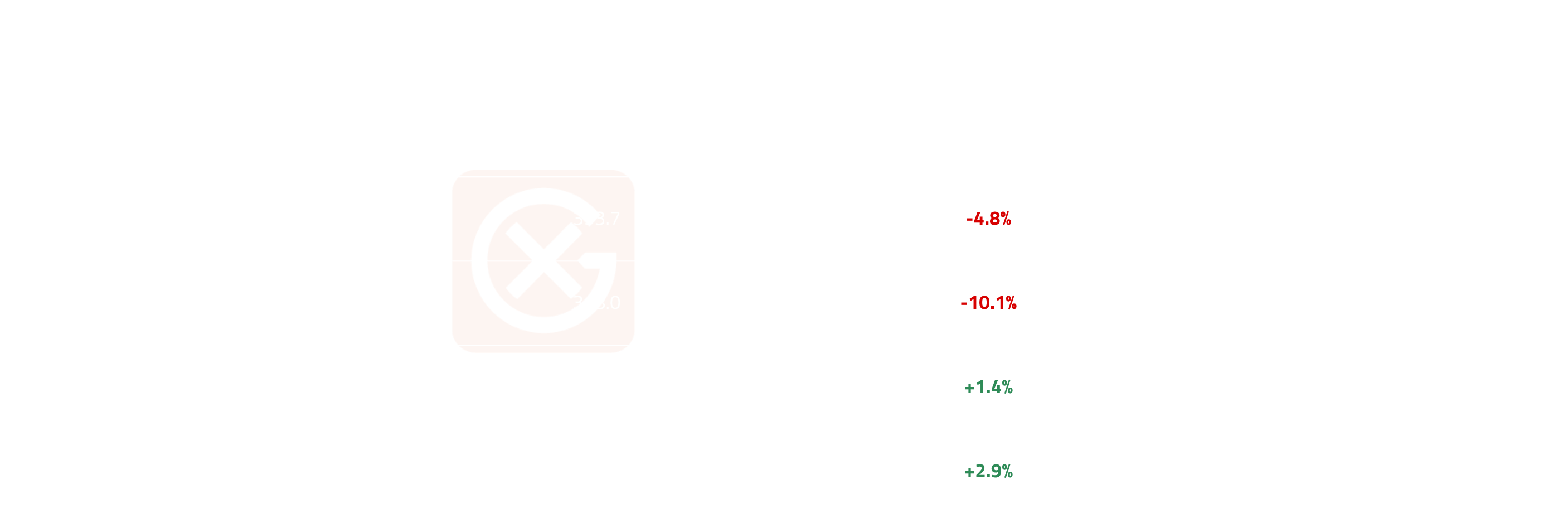

- With Middle East diesel and jet exports still constrained, the ULSD-WTI Houston crack averaged $61.2/bbl (-4.83% MoM, +119% YoY) while flat diesel fell 13.2%.

- The March crude spike unwound faster than diesel, so the crack eased month by month ($70 to $64 to $64 to $61.2) but stayed extreme, closing $66.4/bbl vs $61.1 open as Europe and Asia kept bidding US product above crude.

- ULSD-Brent crack averaged $58.0/bbl (+1.36% MoM), confirming distillate-specific strength; Jet-WTI Houston crack averaged $49.7/bbl (-7.4% MoM), about $11/bbl under diesel.

Cross-regional Dynamics

- Jet 54 Colonial Pasadena averaged 300.0 cpg, down 16.6% MoM against Colonial Pasadena ULSD's 13.2%, underperforming through summer aviation pull.

- The jet-ULSD spread (both legs Colonial Pasadena) deepened -16.9 to -41.0 cpg (avg -32.8, +40.4% MoM), counter-seasonal through peak flying season; a swing back toward jet is the risk.

- Colonial Linden-Pasadena basis compressed to 9.9 cpg avg (-4.71% MoM): no line-space premium building for Gulf-to-East flow.

Curve Structure

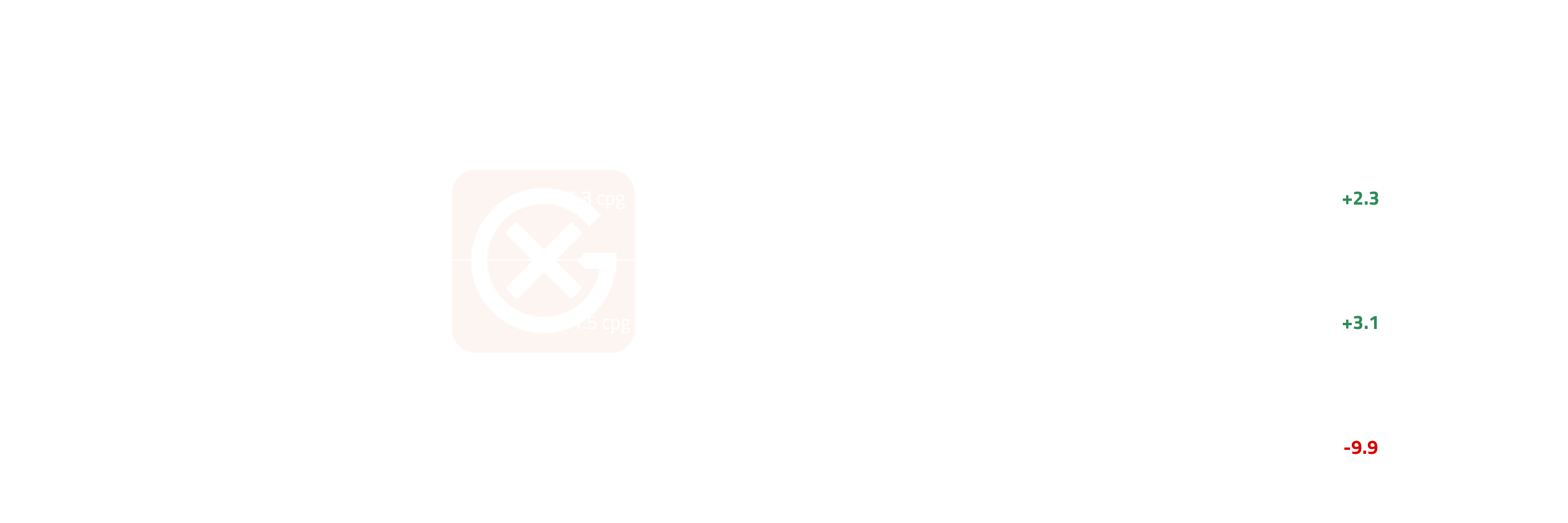

- M1-M2 widened as flat price fell, prompt tightness intensifying while the tape sold off, consistent with stocks about 10% under the five-year average.

- M1-M12 flattened 9.9 cpg as the back fell less than the front, yet the curve stayed firmly backwardated with no shift toward contango.

Price Volatility

- ULSD NYH CV of 6.77% sits below the March 12.73% peak: a directional decline as tension eased, not a fresh shock.

- Crack CV 7.60% and NYH CV 6.77% are the new baseline, not the 4.4-4.5% May prints; anyone still pricing hedges off May is under-hedged.

Something To Watch

- ULSD-WTI Houston crack easing from its extreme: averaged $61.2/bbl (+119% YoY), down from the March $70 peak but still double a year ago. Why it matters: reversion toward $45-50/bbl confirms the froth unwound; holding above $60 confirms Hormuz and Russian-supply tightness persists. Monitor: weekly crack close vs the gasoline crack; EIA Wednesday PADD 1 / PADD 3 distillate stocks.

- Jet-ULSD spread at -41.0 cpg into flying season: deepened through peak summer aviation demand. Why it matters: jet trading this far under diesel in flying season is counter-seasonal; a move back toward flat signals aviation demand re-bidding the molecule. Monitor: TSA daily throughput; jet-ULSD spread close; jet vs diesel crack spread.

- Front-end backwardation firming as flat price falls: M1-M2 widened to +8.6 cpg while flat diesel fell 13.2%. Why it matters: prompt tightening against a falling tape means physical scarcity from thin stocks, not carry; north of 10 cpg prices acute PADD 1 tightness. Monitor: weekly M1-M2 close; Colonial Line 16 line-space premium.

Note: All figures, prices and market activity referenced in this report are based on the period 1 to 30 June 2026.