June split the biofuels complex into two stories. Ethanol drifted lower on ample supply and falling gasoline prices, while RINs climbed steadily as tough new federal mandates met a tighter pool of qualifying feedstocks. That divergence stood out most in the ethanol-gasoline-RIN relationship, where compliance demand looked like a stronger price driver than actual blending costs. On the diesel side, Renewable Diesel California swung sharply before settling higher, while biodiesel pricing nationally stayed flat, so the real action came from RINs and renewable diesel rather than biodiesel itself.

Price Trends

Feedstock Trends

Cross-Commodity Dynamics

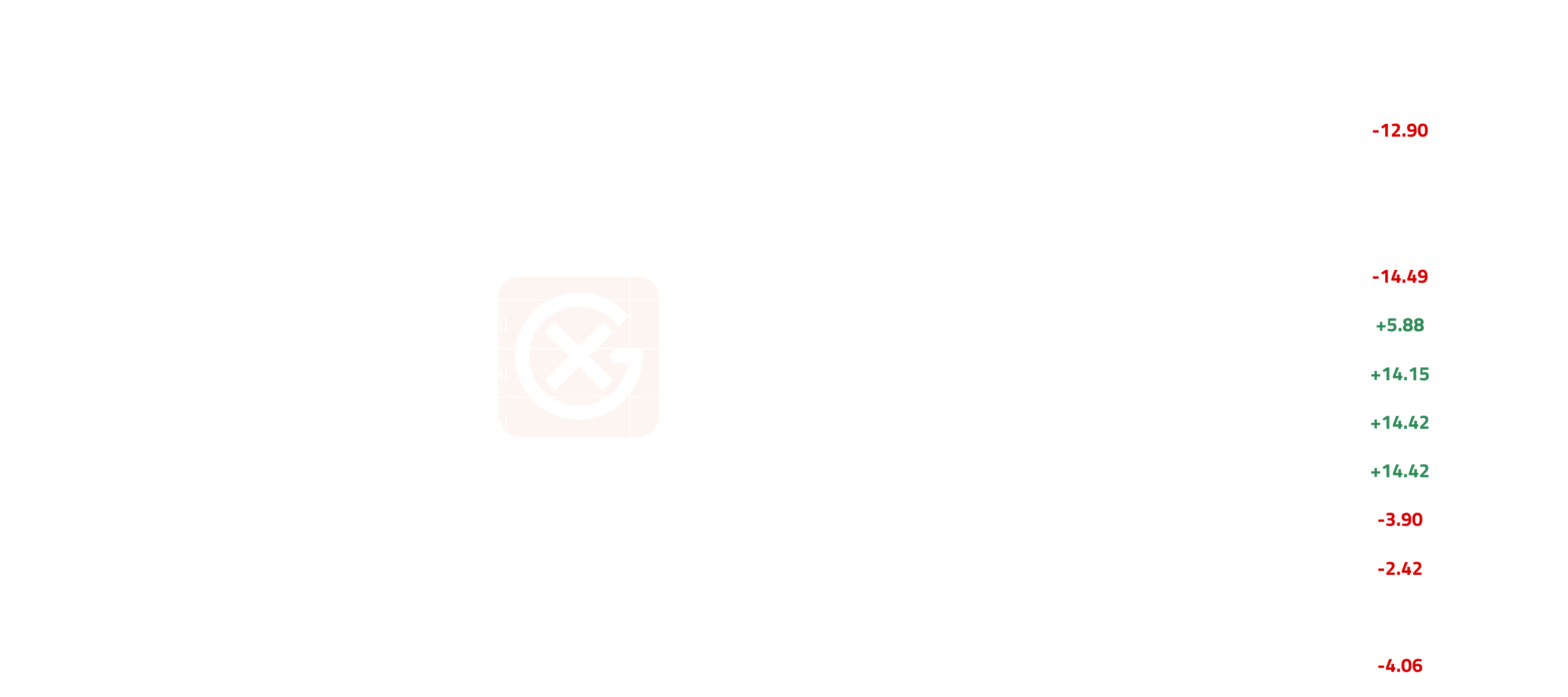

- Gasoline prices fell much faster than ethanol in June, while the D6 RIN moved the opposite way and climbed higher. This is a sign that compliance demand for RINs is now driving prices more than the actual cost of blending gasoline and ethanol together.

- Renewable Diesel California fell while the D4 RIN rose, narrowing the gap between the two sharply.

Market Activity

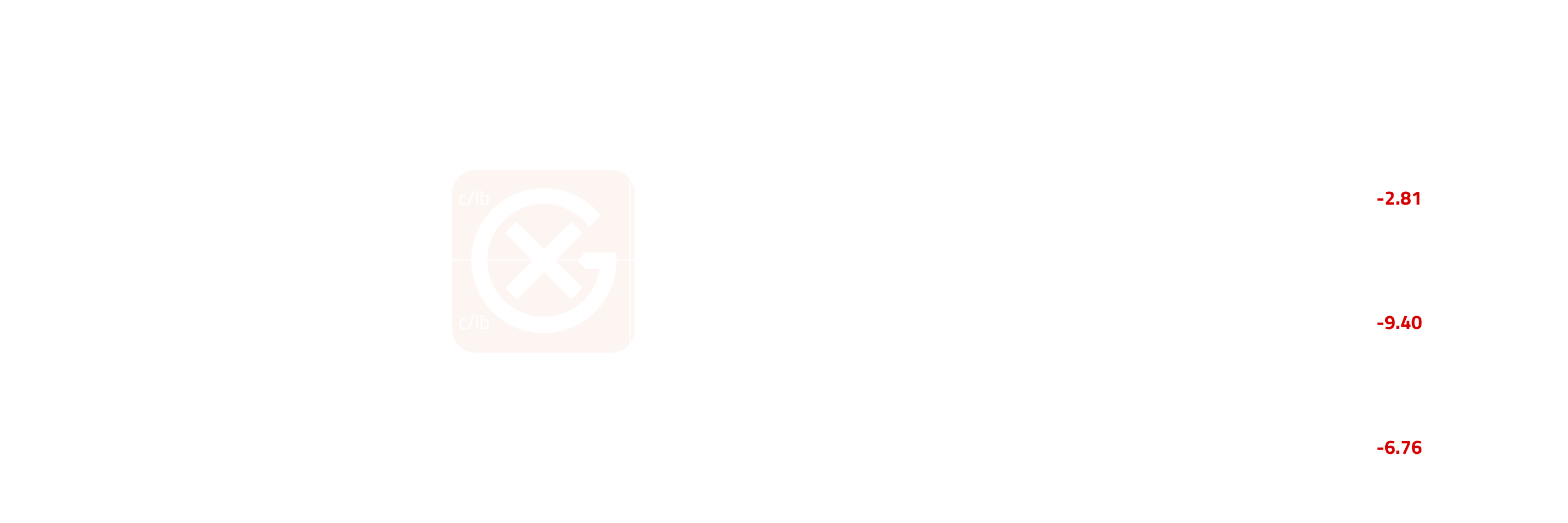

- Prices drifted lower in June. Supply stayed plentiful while gasoline blending demand softened a bit, pulling values down across the board.

- Prices swung sharply up and down during the month before settling higher. Softer feedstock costs, like soybean oil and used cooking oil, weighed on the broader move.

- RIN prices rose steadily through June as the RFS Set 2 rule came into force on June 15, setting record federal blending mandates and pushing compliance costs higher. The 45Z tax credit's restriction on foreign feedstocks, effective from January 2026, further tightened the pool of qualifying supply by limiting credit eligibility to North American-origin oils and fats.

Curve Structure

- The renewable diesel curve is in backwardation, with near-term contracts priced higher than longer-dated ones. The whole curve moved up together in June, though the back end gained slightly more than the front.

- Both ethanol markets in Chicago and NYH are in backwardation as well, with near-term months priced above longer-dated ones. The whole curve fell in June, and since the back end dropped more than the front, the backwardation widened slightly.

Something To Watch

- 45Z clean fuel production credit, final regulations pending: Proposed regulations were published in February 2026 with a public hearing held on May 28, but final rules have not yet been published. Once finalized, the rules will determine exactly how the foreign feedstock restriction is enforced and which emissions methodology producers must use, directly affecting which fuels qualify for the credit and at what value, with knock-on implications for RIN pricing and renewable diesel and biodiesel production economics. Monitor publication of the final 45Z regulations in the Federal Register and the updated 45ZCF-GREET emissions rate table for 2026.