European gasoline cracks have hit their highest since late 2023. In mid-November, ARA gasoline barges traded in the spot market at their highest premiums to the front-month swap since that period, highlighting a market where firm demand is running head-first into constrained supply.

During a recent General Index & Sparta webinar, Saket Vemprala (General Index) and Jorge Molinero (Sparta) unpacked the drivers behind this strength, connecting movements in spot premiums, refiners’ maintenance schedules, component pricing, arbitrage flows, and the ongoing supply imbalance triggered by developments in West Africa.

.png)

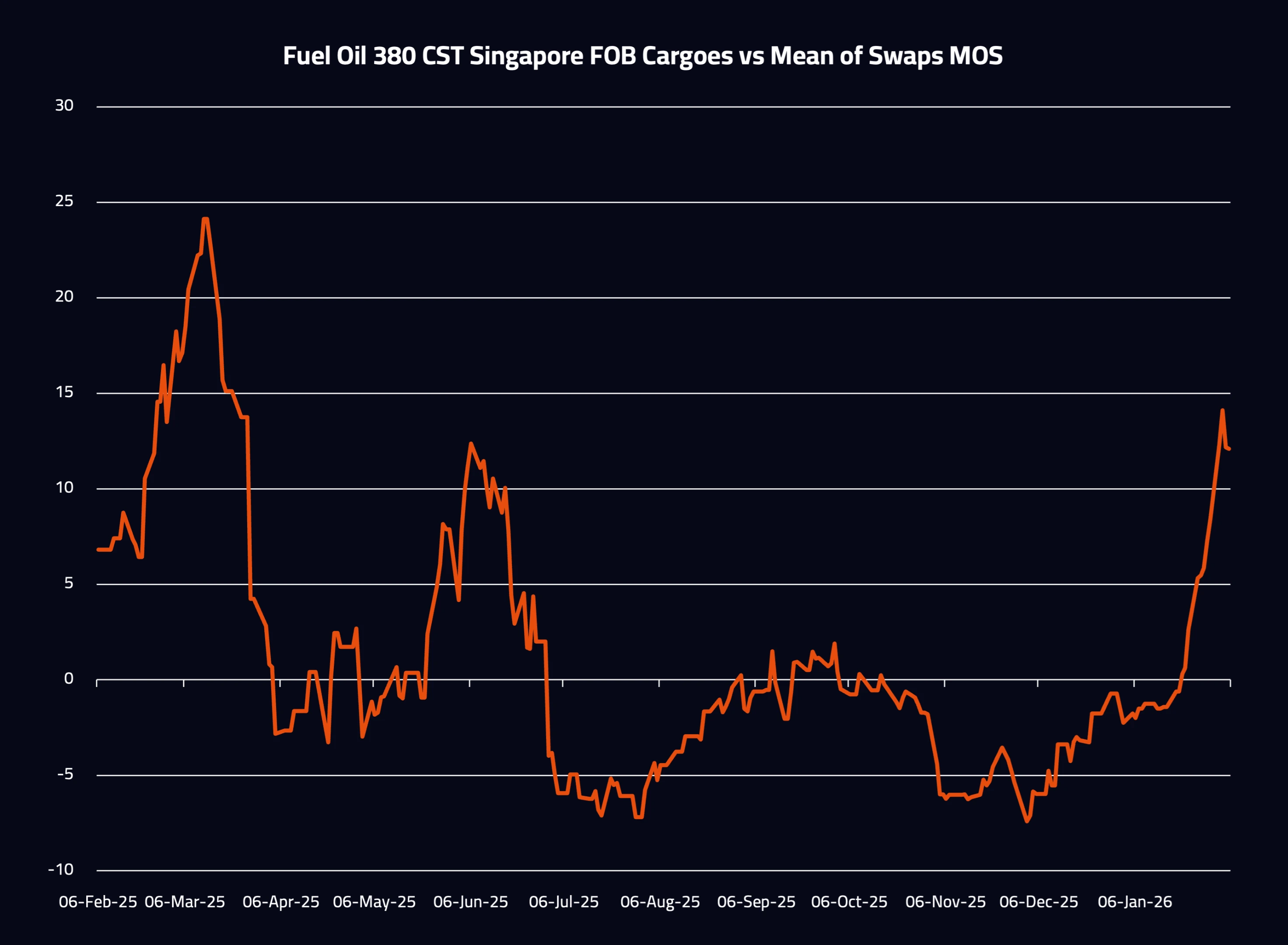

Gasoline cracks rally to multi-year highs

Gasoline cracks in Northwest Europe (NWE) have surged well above the five-year seasonal range, reflecting deep and sustained tightness across the market. The strength is not isolated to the front of the curve - even Q4 2025 cracks remain at historically-elevated levels.

Europe’s outperformance relative to the US and Asia has been striking and is underpinned by:

- Strong gasoline demand for cargoes from ARA

- Persistently low inventories across the Atlantic Basin, especially PADD-1

- Robust diesel cracks resulting in gasoline having to compete to ensure adequate refinery output

Taken together, these factors set the foundation for exceptionally firm gasoline pricing.

Spot barge premiums blow out: a clear seller's market

One of the clearest signals of physical tightness came from the extraordinary spike in ARA gasoline barge premiums. On 12–13 November, some spot trades printed above $80/mt over the front-month swap - levels rarely seen in recent years.

Typically, ARA barges trade at low-to-mid double-digit premiums. The sudden shift into unusually high premia indicates a physical market where buyers had little choice but to chase barrels.

Price action analysis from the day’s trading activity showed buyers aggressively raising their bids - sometimes by $30–35/mt in a matter of minutes or hours - to secure supply. Sellers, meanwhile, conceded very little, underscoring just how tight prompt availability had become.

Supply-side stress: maintenance, outages, and structural losses

European refinery throughput has been materially constrained in 2025. A cluster of outages and structural reductions has curtailed gasoline supply:

- Total Antwerp: major turnaround extended into January 2026

- Shell Pernis: planned maintenance from September through November

- Preem (Sweden): reduced throughputs

- UK: cumulative effects of the shutdown of Grangemouth and Lindsey refineries in 2025, cutting national refining capacity from six to four plants

With multiple outages concentrated in NWE, ARA imports of gasoline and components have weakened noticeably, according to Vortexa.

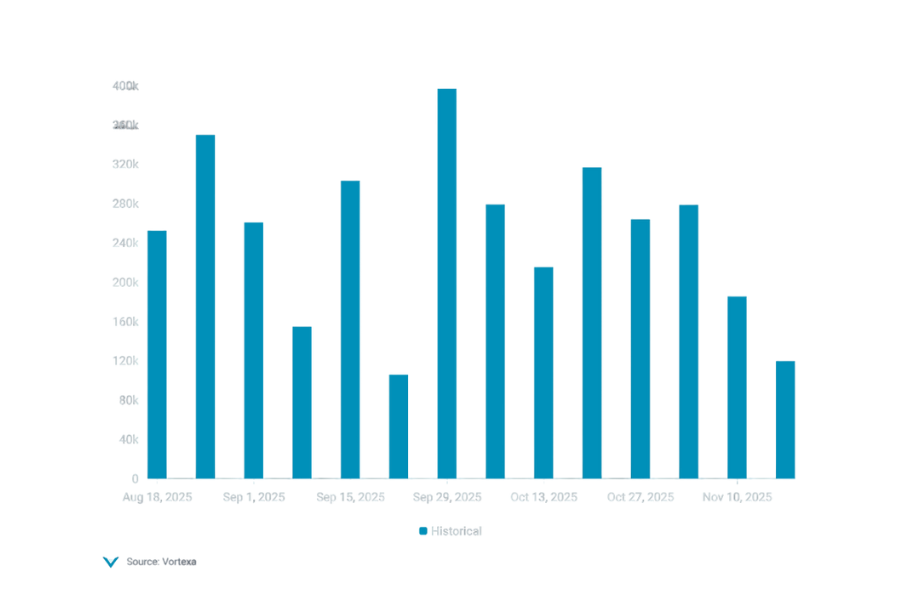

West Africa: the critical pull on European supply

While supply tightness explains part of the rally, the demand pull from West Africa has been pivotal.

.png)

Over the past five to six weeks, according to Vortexa, gasoline in transit to West Africa has consistently exceeded 10 million barrels in each of the past six weeks, driven by:

- Dangote’s RFCC outage from August–October, and further downtime expected in December and January

- Nigerian buyers securing barrels ahead of a potential gasoline import tariff (now postponed)

- Seasonal uplift from Christmas-related demand

With Dangote underperforming expectations for much of 2025, Europe has been called upon to backfill West African demand - tightening ARA balances considerably.

"Dangote remains the gift that keeps on giving… exports to West Africa have surged to the highest levels of the year.” – Jorge Molinero, Sparta

Blending components surge as margins tighten

The tightness in gasoline is also evident upstream in the components market. Over the past week, several key blendstocks experienced sharp price gains.

Components that showed significant increases (30–50% increases in premiums to the front-month Eurobob swap) include:

- Reformate (99 RON+, 103 RON)

- LCCS

- Toluene/Xylene (TX)

- Winter non-oxy gasoline

A combination of refinery outages and the need to blend up barrels for growing demand has forced buyers toward the spot component market, pushing prices materially higher.

According to Sparta, E5 blending margins briefly opened but quickly shut again as components tightened. E10 margins remain workable only at the very prompt, and at far weaker levels than earlier in the quarter.

Arbitrage flows: Europe prices itself out of the Atlantic Basin

Another striking feature of the current market is Europe’s loss of export competitiveness, even as domestic fundamentals tighten.

- Transatlantic arb at record lows

- East/West spread at record lows

- TC2 freight high and rising

- Houston gasoline pricing cheapest into almost all Atlantic Basin destinations except Nigeria

This means Europe cannot meaningfully offload surplus barrels through arbitrage. Instead, West Africa is absorbing volumes that would otherwise have moved trans-Atlantic, reinforcing the tightness in ARA.

Where is the EBOB ceiling?

Despite strong RBOB and Singapore 92 benchmarks, EBOB continues to outperform, driven by a uniquely tight European balance.

.png)

Q1 2025 EBOB cracks are trading about $6/bl above last year’s already-record levels. Support for elevated pricing includes:

- Refinery maintenance and structural closures tightening European supply

- European gasoline demand running 10% above pre-Covid levels

- US gasoline and product stocks at seven-year lows

- Persistent strength in diesel, jet, and naphtha cracks

- Continued tightness from West African imports

The result: a gasoline market that remains fundamentally undersupplied well into early 2026.

“The whole Atlantic Basin is tight. Until stocks rebuild, cracks will struggle to move lower.” - Jorge Molinero, Sparta

Q1 2026 outlook: tightness persists

Even as some refineries return from maintenance, the balance will remain stretched:

- Pernis and Preem coming back online will help, but Antwerp’s extended turnaround and Dangote’s scheduled downtime through December–January will limit stockbuilding

- Low US inventories will continue to support global tightness

- PADD 3 and Mideast Gulf refiners may gain marginal share into global shorts as ARA stays expensive

With structurally constrained supply and broad refined product strength, the European gasoline market is poised to remain at elevated pricing levels through Q1 2026, barring an unexpected rise in availability.

The surge in European gasoline premiums is the product of multiple reinforcing pressures: refinery outages, structural capacity losses, strong European demand, tight US inventories and a large draw from West Africa. Arbitrage imbalances have trapped barrels within the region, magnifying local tightness.

With key refinery units offline into early 2026 and major demand centres still pulling hard on European supply, the market remains fundamentally supported. Barring a rapid reversal in global stock levels, tightness is likely to persist into Q1 2026, keeping cracks and premiums elevated across the gasoline complex.

%20(1).webp)

.webp)

.webp)