Global jet fuel prices have soared by near unprecedented levels in reaction to supply disruption in the Mideast Gulf, following US-Israel strikes against Iran and the retaliatory measures which have closed the critical Strait of Hormuz.

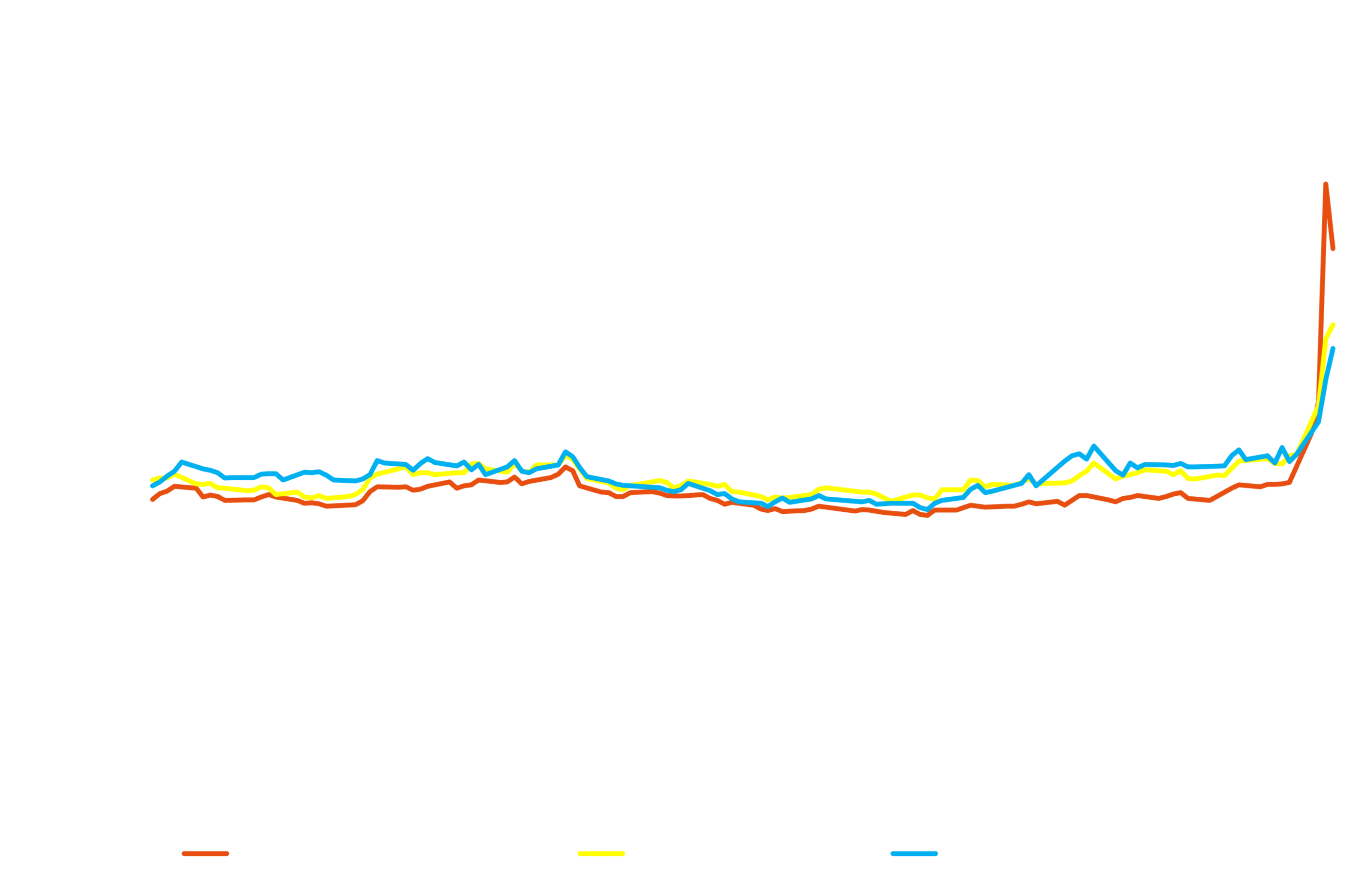

- Jet Fuel Singapore FOB Cargoes soared significantly 137% from $736.61/MT (27-Feb) to $1,744.71/MT (4-Mar), with the sharpest move (+72.94%) concentrated on the 4th of March before a slight dip on 5th Mar to $1526.74/MT.

- On the other side of the Suez Canal, Jet Fuel NWE CIF Cargoes advanced 53% over the same period ($831.00/MT to $1,268.75/MT).

- In North America, Los Angeles Jet added 57% to reach $1,273/MT while New York Buckeye rose by 47% to reach $1,189.25/MT.

- The last time jet was seen permeating such levels was June 2022, following Moscow’s invasion of Ukraine and the resumption of air travel demand post COVID-19.

Refining margins at both ends of the hemisphere surged in tandem with flat prices, a clear sign that the rally in crude was not the sole reason for the uptick in jet prices. With stronger regrade levels in both Singapore and Northwest Europe, it is indicative that jet is more susceptible than the other refined products, to supply disruptions caused by the US-Iran war.

Why has the growth of jet fuel outpaced the other products?

Since the implementation of the 18th sanctions package on Russian-origin refined products, Europe has limited its options to derive middle distillates exports from. Between the implementations of sanctions on February 21st and the outbreak of the US-Iran war on February 28th, Europe received 301.63kbpd of jet fuel from the Middle East, equivalent to 61.8% of their total jet imports during the same period, according to data from analytics company Vortexa.

The outbreak of the US-Iran war restricts the options Europe has left to import the aviation fuel, raising the need for arbitrage opportunities to open between Europe and the Americas or Asia.

Asia which is typically a net exporter of conventional jet fuel faces possible supply disruptions of its own. The Hormuz situation leaves the continent’s refiners struggling for replacement crude options and with most only having a week’s worth of crude in stock and no clear end insight to the war, refiners will have to execute run cuts or risk having to shut their plants down when their crude stockpile runs out. Plant shutdowns may incur unnecessary operational costs and downtimes should the war end earlier than they expect.

Refiners such as MRPL have declared force majeure on upcoming exports while Chinese refiner Zhejiang Petrochemical Corp have brought forward maintenance to mitigate the current circumstances. Thailand and China have also begun suspending oil exports to protect their own oil reserves.

.png)

.webp)