.webp)

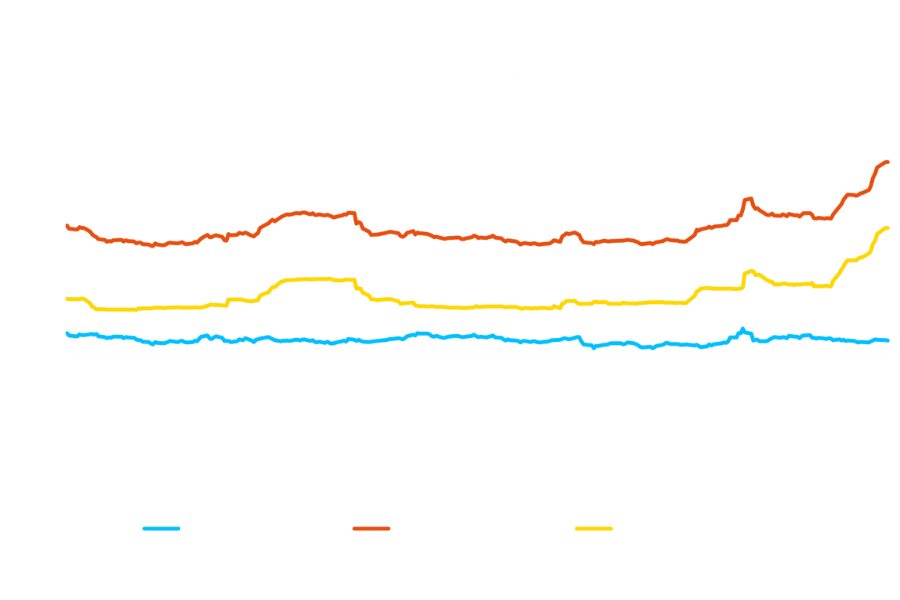

- NWE SAF price highest since March 2024

- SAF premium widens to 3.7x vs Jet Fuel

- HEFA-SPK margin rallies, UCO stable

- SAF regains top spot over HVO

If you’ve flown from one of Europe’s main aviation hubs on vacation over the summer, there’s a chance some of the fuel powering your flight was of the SAF variety – that’s to say a fuel produced from waste feedstocks such as used cooking oil or animal fat.

Since the introduction of EU and UK mandates in January, aviation fuel suppliers have been obliged to start blending 2% SAF into the conventional jet fuel streams.

SAF is more expensive than regular jet fuel. Unless the airline applied a SAF surcharge or gave you the chance to offset emissions, however, you probably won’t have noticed any difference in cost this year. That could change if recent price trends in the nascent SAF market fuelled by mandate demand and tighter demand and tighter supply are a sign of things to come.

NWE SAF price reaches 3.7x cost of jet fuel

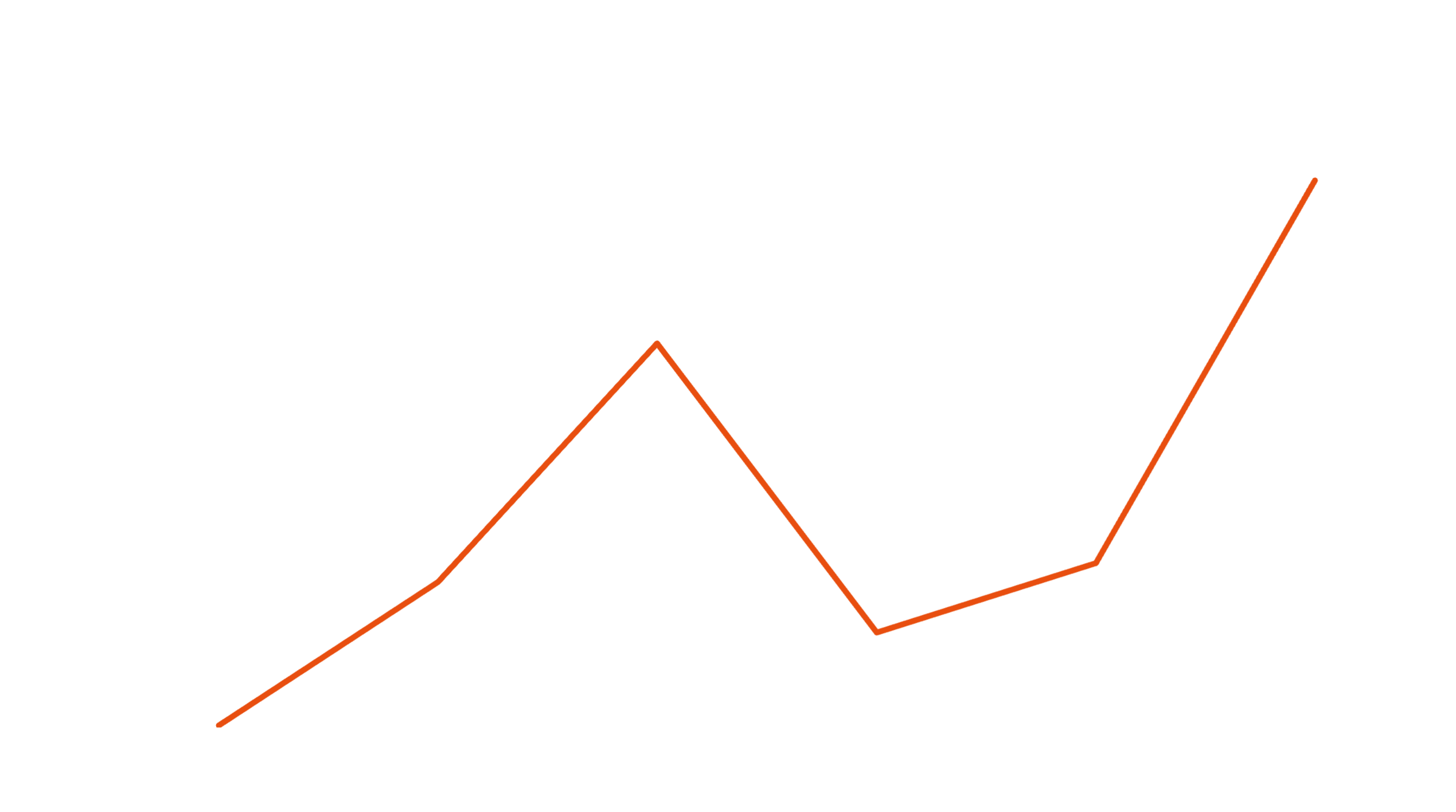

According to General Index (GX) data, the price of SAF in Europe has soared by nearly 30% in August. The index price for Neat SAF FOB Barges in Northwest Europe was calculated by GX at $2631/ton on 28 August – an increase of $570 this month.

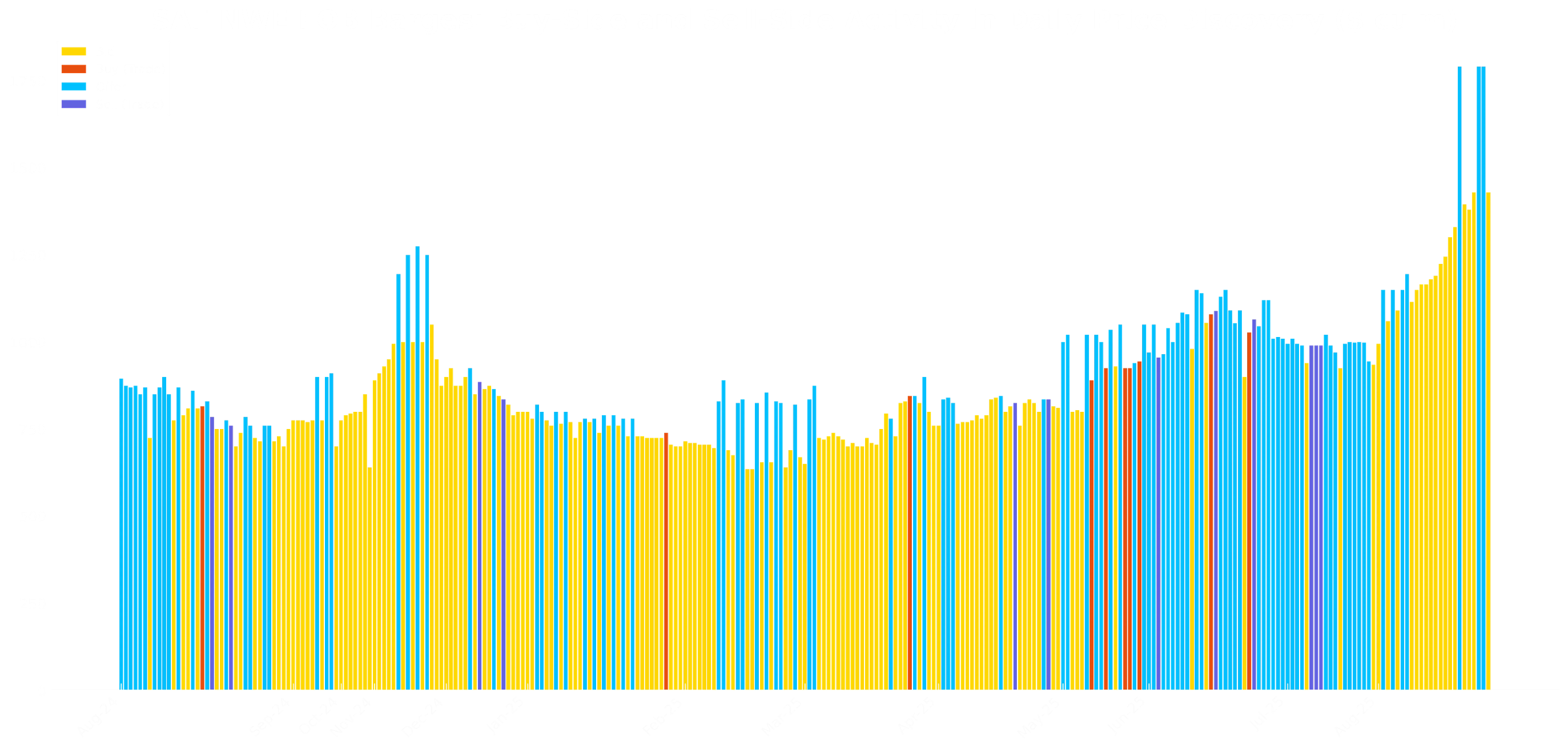

Buy-side spot market activity drives SAF gains

From an index rationale perspective – i.e. purely a trade data explanation – the price rally has been driven by strong buy-side action in the spot market. Based on activity in daily price discovery sessions, after seeing Gunvor on the sell-side at the start of August, Shell was then active as the solitary participant bidding for barges over 10 sessions. Bid levels increased by 44%. The rally didn’t entice offers back in until the eleventh session, when Petroineos was recorded offering. No trades occurred. The rally has cooled a little this week; but, if it’s only paused for breath, the latest offers could point to SAF heading above $3000/ton – territory the market’s not been in since Nov 2023.

A quick explainer on this chart: we’ve plotted in chronological order the trading activity (bids, offers and transactions in dollar per cubic metres) aggregated by GX. We convert these levels into dollars per metric tons as part of the calculation logic for our final index. For more on our SAF Neat HEFA NWE FOB Barges methodology, here’s the index factsheet.

Waste oil feedstocks broadly stable despite global disruption

The underlying UCO and tallow feedstocks markets have been relatively flat this month compared to SAF. Global UCO prices do not yet appear to have been substantially affected by US policy changes around incentives for domestic producers and new requirements on feedstock sources. If the US imports less UCO from Asia, this supply can be redirected to other destinations which might be offsetting bullish price impact from an reduction in UCO exports from China so far this year.

NWE SAF margin up in boost for HEFA producers

For SAF producers, stable feedstock and higher product prices should translate into stronger margins. A simple HEFA-SPK margin is now around $900/ton by our calculation – music to the ears of Neat SAF producers in Europe (and their investors), who had endured a period of weaker margins. If feedstocks prices are broadly stable, end product supply & demand fundamentals offer a clearer explanation for SAF’s performance.

UK SAF blending progress suggests supply lagging mandate

Recent data published by the UK government showed SAF blending ratios lagging behind the 2% target at the half-way point of the first mandate year. SAF deliveries as a share of total aviation fuel supplied averaged 1.345% over Jan-Jun. While we can only speculate about exact progress in the EU, it’s safe to say aviation fuel suppliers will now need to enter the spot market with greater urgency to source outstanding volumes. Non-compliance penalties apply under the flagship ReFuelEU mandate policy, while a buy-out price is an option under the UK scheme.

NWE SAF regains premium over HVO, but supply easing not a given

.png)

On the supply side, the interplay between SAF and Renewable Diesel has been negative for aviation fuel output. Both products are produced from HEFA refineries and RD (aka HVO) prices have been stronger than SAF for several months, resulting in refiners prioritising the road fuel.

Reduced SAF supply resulting from these refinery dynamics could be a contributing factor in SAF’s recent rally. But the relationship has now flipped. SAF’s moved from a discount to a chunky premium over RD. If this trend continues, refiners should be incentivised to produce more SAF.

However, theory doesn’t always translate into practice. Domestic refiners in Europe with RD commitments to meet no longer have the option to resupply their renewable road fuel requirements from Asia without restriction due to EU antidumping measures, so we may not see SAF runs increased across the board.

The restrictions on RD imports from Asia do not exist for SAF, so its price surge, again on paper at least, improves arbitrage opportunities from Asia into Europe. Shipping data seen by GX suggests there was a lull in SAF cargoes ex-China with August laycans (loading dates). Reports say Chinese producers are stalled waiting for export quotas. Assuming they come, if there are unplaced SAF cargoes originating in China – or for that matter ex-Singapore or Malaysia – traders won’t hang about to capitalise on stronger returns to meet regional European mandate demand.

We’re also seeing SAF being shipped from the United States to Europe. The volumes are sparse compared to more regular flows ex-Asia, but in nascent SAF trading markets the transatlantic arbitrage is also going to be one to keep an eye on.

Will SAF spot strength narrow gap to 'compliance fee' for airlines?

Airlines with exposure to variable SAF costs terms won’t welcome the prospect of fuel procurement invoices soon landing from their supplier with a sharply higher cost to pay.

No doubt speculation over the justification for higher prices will be heightened at airline HQs, wondering whether suppliers – some whom can produce a ready-blended SAF Jet Fuel at their oil refineries by adding waste oils like UCO into the processing systems – are unfairly pocketing large margins in the form of so-called ‘compliance fees’.

The International Air Transport Association (IATA) published research at the start of the summer which put the “Implied SAF Price” charged to airlines as part of these fees between $3,000-3,500/mt. This data was for the first half of 2025, when the SAF NWE FOB Barge spot market price was calculated by GX in a range of $1,750-1,900/mt.

Sign Off: As mandates are rolled out beyond Europe as expected in the coming years, recent SAF price trends are surely a reminder airlines won’t be able to avoid passing on the green fuel premium to passengers unnoticed forever. Your next summer holiday may need to budget for the SAF cost too!

%20(1).webp)

.webp)

.webp)