Bullish sentiment swept through Brent-related spot and forward instruments in reaction to military action in the Middle East.

- Front-month ICE Brent settlement rose more than $5/bl on the day to 2 March, to $77.74/bl – the highest since June 2025.

- Within the weekly Brent CFD market:

- Contango structure narrowed: Week 1’s discount to Week 4 narrowed to -$0.41/bl on 2 March, compared to -$0.73/bl the previous day.

- The number of trades fell to 72, from 97.

- Traded volumes fell to 7,500 bl, from 10,100 bl.

- The proportion of buyer- and seller-initiated trades did not significantly change day-on-day.

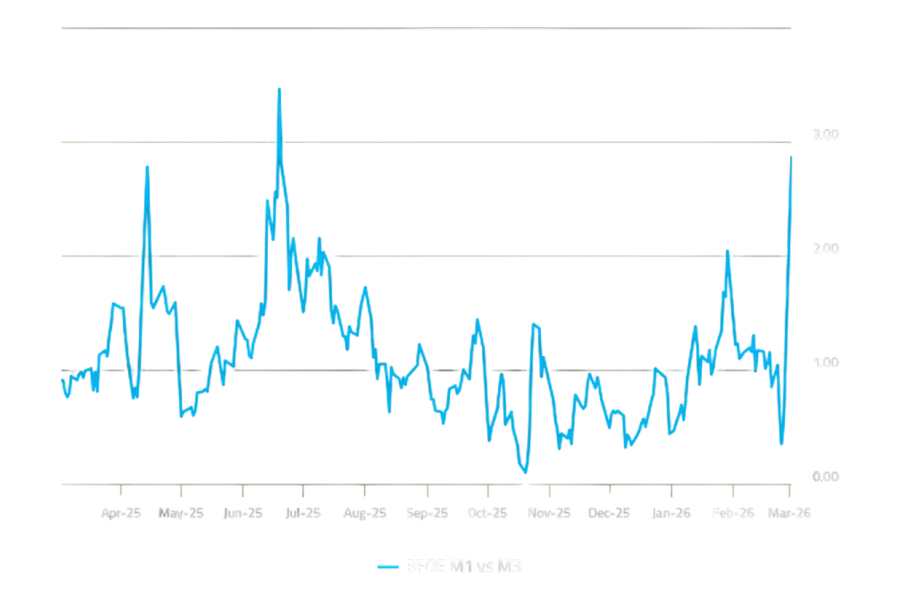

- In the Cash BFOE market: front-month soared to a +$2.86/bl premium to the third-month contract – the highest since June 2025:

- Dated Brent rebounded to a +$1.26/bl premium to second-month Cash, having come under pressure in the previous week .

- The Dated Brent forward curve also showed a steepening of backwardated structure on the first trading day after the outbreak of hostilities:

.webp)

- On physical grades, fresh buying interest was concentrated on medium sour Johan Sverdrup crude: Neste and Equinor both bid for cargoes on 2 March.

.png)

.webp)