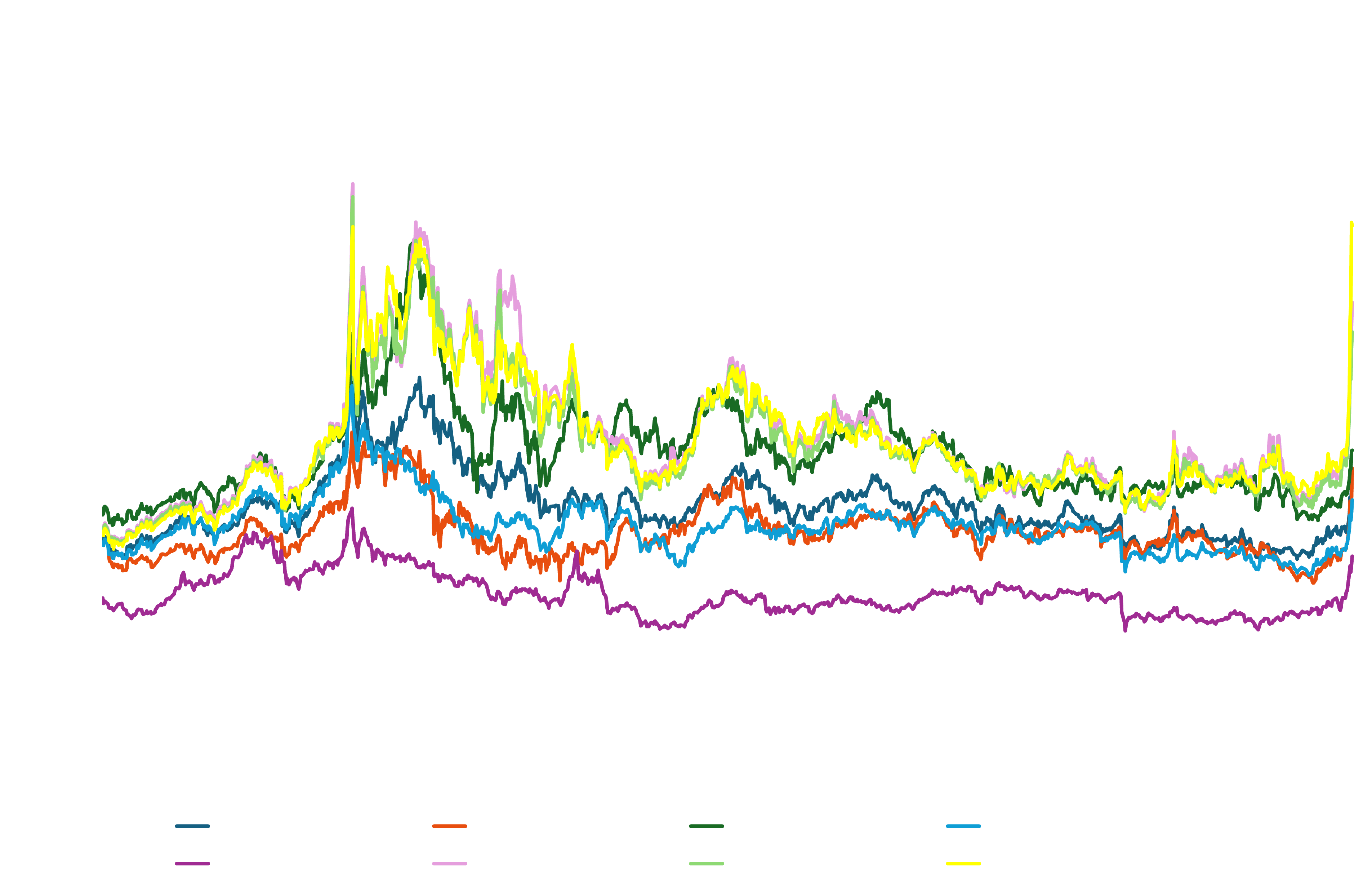

European oil pricing surged to multi-year highs and highest-ever levels on some metrics in the week-ending 6-March, following seven days of military action by the U.S.-Israel against Iran. Retaliatory measures by the Islamic Republic has choked off the transit of feedstocks and fuel through the Strait of Hormuz, squeezing normal supply exports to consumers in Asia, Americas and Europe. Iran has also knocked out major oil infrastructure across the Mideast Gulf, including several of the world’s largest refineries, key ports, and storage terminals - adding to the disruption, and setting the tone for highly bullish, volatile market activity.

Market prices at the start of trading of Monday, 9 March reached fresh highs and remained volatile. During Asian trading, ICE Brent Crude Oil Futures opened around $101-102/b then rallied to $118/b before falling back towards where it had begun. ICE LSGO (Diesel) Futures opened around $1,252/MT (equiv $167.82/b), rose above $1,380/mt ($184.97/b) before falling to around $1,240/mt ($166.21/b) by noon in Europe.

All prices sourced from GX proprietary indices, assessed at 16:30 London time. Last published data point: 6 March 2026.

Core Pricing

WTD change measured 27-Feb to 5-Mar. Jun '25 High: intraday peak assessed by GX, all products peaking 19 June 2025 (Propane: 23 June).

North Sea Crude

Dated Brent FOB NWE (GX0000968)

- Regional Price Reaction. Dated Brent surged $23.48/bbl (+33.1%) across the week, closing Friday at $94.31/bbl - its highest assessed level in over two years and the single largest weekly gain in recent memory. Friday's $6.39/bbl advance (+7.3% on the day) was the strongest daily move of the week, signalling that the market closed with conviction rather than fatigue. The week's trajectory was characterised by an initial step-change higher on Monday as the weekend’s military operations were incorporated, a further acceleration mid-week, a brief $3.60/bbl retracement on Wednesday as participants tested the durability of the Hormuz closure, and then a two-session surge into the close. The North Sea physical differential held firm throughout, with Forties and Ekofisk premiums widening as Atlantic Basin supply was called upon to partially backstop dislodged Gulf volumes.

- YTD Context. The market opened the year at $60.85/bbl, posting gains of just over $10/bbl through January and February before the geopolitical premium exploded in the current week. The YTD advance of $27.07/bbl (+44.5%) has compressed the year's trading into a dramatically narrow range: nearly two-thirds of that gain has been recorded in a single trading week. At $87.92/bbl, Brent has broken decisively above the $80/bbl threshold that capped rallies through much of 2025, transforming the technical picture meaningfully.

- June 2025 Comparison. The June 2025 military escalation - the prior U.S.-Israel strike campaign - drove Brent to an intraday high of $80.60/bbl on 19 June 2025, a level that was rapidly surrendered once a ceasefire framework emerged within 48 hours. The current episode has already exceeded that peak by more than $7/bbl and, critically, the physical closure of the Strait adds a structural supply dimension absent in June. In June, price action was driven almost entirely by risk premium in the paper market; this week the physical market has also fractured, with CIF assessments for Atlantic Basin grades now trading at multi-year highs on genuine cargo scarcity.

- Forward Curves. The prompt/prompt +1 spread has blown into steep backwardation across the forward curve, with the front of the Brent complex in sharp contango inversion. M1/M2 backwardation has widened from circa $0.30/bbl pre-crisis to levels not seen since the post-Russian invasion squeeze of 2022. The back end of the curve (2027 onwards) has moved by a fraction of the front-month premium, implying that market participants expect either are solution or significant demand destruction to re-establish equilibrium - a view consistent with June 2025 precedent but fragile given the degree of infrastructure damage now reported.

Middle Distillates

ULSD 10ppm CIF NWE (GX0000093) | ULSD 10ppm FOB Barges (GX0000095) | Jet Fuel CIF NWE (GX0000015)

- Regional Price Reaction. Middle distillates dominated the week's price action, with ULSD CIF NWE closing Friday at$1,207.75/mt - a $445.25/mt weekly gain (+58.4%) that breached the $1,000/mt psychological threshold on Tuesday and kept running. Friday alone added $66/mton the CIF assessment, maintaining the pace of the broader crude-driven rally. The CIF/FOB barge spread widened significantly to $57.25/mt by the close, versus $34.50/mt on Thursday, reflecting intensifying freight and insurance premiums on seaborne cargoes as cargo-route disruption deepened. Jet fuel was the week's standout product in absolute terms, closing at $1,517/mt for aweekly gain of $686/mt (+82.6%), though it was the sole decliner on Friday - slipping $11/mt as near-term aviation demand concerns briefly offset the supply premium.

- YTD Context. ULSD CIF NWE opened 2026 at $619.25/mtand gained around $143/mt through January and February in a measured firming. The week's $445/mt surge has multiplied that prior YTD gain more than threetimes over in a single week, taking the total 2026 advance to $588.50/mt(+95%). At $1,207.75/mt, diesel is approximately $382/mt above its June 2025 intraday high - a stark measure of how structurally more severe this disruption is relative to the prior escalation. The gasoil-crude crack spread, which averaged sub-$12/bbl through early 2026, closed the week at extraordinary levels well north of $20/bbl. Jet fuel's YTD gain of $844.75/mt represents a near-doubling of the January opening price.

- June 2025 Comparison. The June 2025 episode drove ULSD CIF NWE to an intraday high of $826/mt and Jet to $843.50/mt on 19 June - moves that retraced by roughly $130–135/mt within five sessions as the situation stabilised without physical supply disruption. Current week closing prices exceed both those prior peaks by margins of $382/mt (ULSD) and $673.50/mt (Jet) respectively. The qualitative difference is fundamental: multiple large-scale refinery complexes in the region are reported offline, storage terminals at key Gulf hubs have been struck, and physical supply of product into European loading programmes is visibly curtailed. June 2025 was a sentiment trade; this week is a fundamentals trade, with the Friday close confirming the market has not yet found a ceiling.

- Forward Curves. Gasoil and diesel forward structures closed the week in extreme backwardation, with near-dated swaps at elevated levels while deferred months moved far more modestly - creating a steeply inverted curve that signals acute prompt-end stress. The ICE Low Sulphur Gasoil term structure shows the sharpest front/back premium in years.

Light Ends

Naphtha CIF NWE (GX0000092)

- Regional Price Reaction. Naphtha CIF NWE gained $46.25/mt (+6.6%) onFriday to close the week at $743.75/mt - a weekly advance of $156/mt (+36.2%). While the percentage gain was more modest than distillates or crude, the absolute trajectory is significant: naphtha has reached its highest assessed level in at least two years. The market benefited from a dual driver: the underlying crude price surge pulled naphtha higher as a crude derivative, while petrochemical feedstock demand from European crackers - seeking to substitute Middle Eastern condensate and straight-run naphtha supplies now disrupted - added a product-specific premium. Asian demand for European-origin naphtha was also reported picking up as East Asian buyers sought Atlantic Basin alternatives for disrupted Gulf cargoes.

- YTD Context. Naphtha opened the year at $477/mt, gaining approximately $110/mt through January and February in a steady grind higher consistent with the broader energy complex firming. The week's $110/mt gain has essentially doubled the year-to-date prior gain in five trading sessions, bringing the YTD total to $220.50/mt (+46.2%). At current levels, the naphtha-to-crude relationship (the so-called naphtha crack) has moved back towards positive territory after spending much of late 2025 under pressure, offering improved economics for European condensate splitters and simple refiners processing light sweet grades.

- June 2025 Comparison. Naphtha NWE CIF peaked at $620/mt on 19 June2025 during the prior escalation, a level that current prices have now exceeded by approximately $77/mt. Unlike distillates, naphtha's June 2025 reaction was relatively contained - the product is less directly exposed to Middle Eastern refinery output given the diversity of supply origins feeding into NWE. In the current scenario, however, the combination of a much sharper crude move and confirmed disruption to Gulf condensate export logistics has extended naphtha's response well beyond the prior episode.

- Forward Curves. The naphtha forward curve has steepened into backwardation, though less dramatically than distillates - reflecting the more diversified global supply base for light ends and the prospect that alternative supplies from West Africa, the U.S. and Russia-linked routes can fill some of the gap over the medium term. The M1/M3 backwardation has widened but remains narrower than the comparable diesel or jet structure, consistent with fundamentals being tighter but not as acutely dislocated.

Fuel Oil

HSFO 3.5% 380cst FOB NWE (GX0000266) | VLSFO 0.5% FOB NWE(GX0000087)

- Regional Price Reaction. Both fuel oil grades posted solid absolute gains this week, but fuel oil underperformed the broader energy complex in percentage terms - a pattern consistent with its lower sensitivity to direct product supply dislocation. Fuel oil was the most dramatic story in percentage terms on Friday, with HSFO 3.5% 380cst closing at $590/mt after surging $77.75/mt on the day (+15.2%) — the largest single-day move across the entire barrel. VLSFO 0.5% added $55.75/mt (+10.2%) to close at $599.75/mt. The hi-5 spread (VLSFO premium over HSFO) narrowed sharply to $9.75/mt from $60/mt pre-crisis - a counter-intuitive compression driven by HSFO's tighter prompt availability (Middle Eastern fuel oil export cargoes disrupted) outpacingVLSFO's more resilient supply from NWE refiners. Power sector demand for HSFO has also risen as some gas-fired generation is impacted by gas supply uncertainty.

- YTD Context. HSFO opened 2026 at $319.50/mt, the lowest product inthe NWE barrel. Its YTD gain of $192.75/mt (+60.3%) is proportionally the largest across the barrel, though from a lower absolute base. This reflects fuel oil's dual exposure: crude linkage on the upside, and the specific disruption to Middle Eastern residual fuel exports that flow heavily into Asian and European bunkering hubs. VLSFO's YTD gain of $181.75/mt (+50.2%) similarly reflects a strong crude-linked move, though the hi-5 spread compression suggests HSFO has caught up unexpectedly.

- June 2025 Comparison. HSFO NWE peaked at $489/mt on 19 June 2025, a level the current week has exceeded by approximately $23/mt. VLSFO peaked at$523.75/mt in June - interestingly, current prices at $544/mt have now exceeded the prior peak, suggesting the supply disruption impact on marine fuel is more sustained this time around. The hi-5 spread was approximately $35/mt in theJune peak period, broadly similar to current levels, though the path of convergence was different: June saw VLSFO lead higher while this week has seenHSFO close the gap from below.

- Forward Curves. The fuel oil forward curve has moved into backwardation but less acutely than crude or distillates. Prompt HSFO backwardation versus M3has widened meaningfully, driven by bunkering demand at Rotterdam and Antwerp as ship operators scramble to store fuel ahead of potential extended Hormuzclosure. VLSFO's forward structure is similarly backwardated but more gentlysloped, with the market pricing some eventual supply normalisation.Singapore-linked fuel oil trade references have partially disconnected from NW Egiven the Hormuz closure, creating geographical price divergence.

- Liquidity. Fuel oil market liquidity held up comparatively well in the barge marketthrough the week, partly because the product is less exposed to cargo-route disruption for European buyers than crude or distillates. Rotterdam barge activity remained active, though bid/offer spreads widened significantlycompared to the prior week.

LPG

Propane CIF NWE Large Cargoes (GX0000686) | Butane CIF NWE Large Cargoes (GX0000687)

- Regional Price Reaction. LPG prices surged sharply, with Propane CIF NWE closing Friday at $758.75/mt - up $170.50/mt (+29.0%) on the week - and Butane CIF NWE gaining $127.50/mt (+24.8%) to $640.75/mt. The moves are the largest weekly LPG gains in recent memory, driven by the impact of the Hormuz closure on Middle Eastern LPG exports: Saudi Arabia, Kuwait, Iraq and the UAE collectively account for a substantial portion of global LPG supply, much ofwhich transits the Strait destined for Asian and European markets. The propane/butane spread widened to $118.00/mt, reflecting propane's greater exposure todisrupted fractionation output from the Gulf. Domestic European heating demand -still present in early March - amplified spot market tightness.

- YTD Context. Propane opened 2026 at $473.75/mt and butane at $466/mt, with the two products trading in unusually close proximity throughJanuary and February. The pre-crisis YTD gain for propane was approximately $115/mt through late February; the week's additional $170.50/mt has more thandoubled that gain. At $758.75/mt, propane is now trading well above naphtha onan energy-adjusted basis, an unusual premium structure that reflects supply-side dislocation rather than demand-driven fundamentals. The propane-to-naphtha spread has inverted sharply as a result - a rare and significant market signal.

- June 2025 Comparison. Propane NWE CIF peaked at $509/mt in theJune 2025 episode (peaking slightly later than other products, on 23 June rather than 19 June), while butane peaked at $529.75/mt on 19 June. Current week prices have surpassed both prior peaks by substantial margins - propane by approximately $250/mt (+49%) and butane by $111/mt (+21.0%). The asymmetry between propane and butane's performance relative to June reflects the product-specific impact: Gulf fractionation outages disproportionately affect propane export volumes, while butane has partially benefited from substitution into the European gasoline blending pool as refinery operations adjust to thehigher crude price environment.

- Forward Curves. LPG forward curves have moved into sharp backwardation, with the prompt/M3 propane spread at multi-year highs. This reflects the classic response to an acute supply shock: buyers are paying upfor prompt delivery while the market prices eventual normalisation of Middle Eastern LPG flows over the medium term. Butane's forward structure is somewhatless backwardated than propane's, consistent with its more diversified supply origins including NWE refinery output and North Sea associated gas production. Winter demand-driven carry trades have effectively been replaced by scarcity-premium dynamics.

- Liquidity. LPG cargo market liquidity was severely impaired through the week. The majority of large VLGCs that would normally load in the Arabian Gulf fordelivery into NWE and Asian markets are either unable to transit Hormuz or havebeen diverted on extended routes around the Cape of Good Hope, adding 15–20days to voyage times. This voyage-length extension is itself a significantfloating storage of cargo, tightening effective prompt supply further. Seagoing coaster activity in the North Sea remained relatively active as buyers sought to cover near-term requirements from domestic sources, but volumes were insufficient to offset the displaced large-cargo supply.

Analysis compiled using GX proprietary price assessments. Last GX data point: 6 March2026 (16:30 assessment).

.png)

.webp)